Securitization may give you access to gold nuggets when your business is still producing pebbles, but inadequate regulation and other risks can ruin your Midas touch. Richard Li explores the key issues

Suppose your company is running short of money to support daily operations, or maybe further expansion – both quite likely scenarios – where do you find the cash? Banks may be hesitant to lend, a public offering may still be a faraway dream, and the bond market may not open its door to companies without a strong credit rating. But securitization can perhaps work wonders for you.

Securitization was once blamed for causing the 2007-2008 global financial crisis, but with necessary risk control rules in place its basic function of turning illiquid assets into cash in hand can help many in need, especially small and medium-sized companies, when the economy is in the doldrums.

[ihc-hide-content ihc_mb_type=”show” ihc_mb_who=”1″ ihc_mb_template=”2″ ]

Kingsley Ong, a Hong Kong-based partner at Eversheds and secretary-general of the Asia-Pacific Structured Finance Association, says domestic securitization in China is taking off, and “investors are becoming more eager to get exposure to China securitization”.

Ong expects the growth of China’s securitization industry to continue. “China needs to develop its debt capital markets in order to further liberalize and internationalize the CNY currency. Securitization is an essential component of China’s debt capital markets,” he says.

Wang Shengzhe, a Shanghai-based counsel at Hogan Lovells, also foresees more securitization transactions. “The economy in China goes slowly,” she explains. “Small and medium enterprises may have liquidity difficulty, and it can be very difficult for them to obtain loans from banks. The financial institutions will have difficulty to manage their balance sheet and to manage non-performing loans.”

Although details may differ in specific deals, most securitization processes share a basic form: a company, as the originator, identifies income-generating assets to be placed into a pool of underlying assets, which will be sold to an independent special purpose vehicle (SPV) and thus – hopefully – be removed from the company’s balance sheet. Based on the underlying assets and their future income, the SPV then issues asset-backed securities (ABS) to capital market investors. Funds raised from the issuance will be transferred to the originator as payment for purchasing the underlying assets.

A uniform regulatory system has yet to be formed for the asset securitization business in China. The market currently has two popular securitization models. The first is credit asset securitization, subject to the oversight of the People’s Bank of China (PBOC) and the China Banking Regulatory Commission (CBRC). Originators are usually banks or other financial institutions, and the SPV used in this model is usually a trust company. Credit asset-backed securities are offered and traded in the national interbank market, and the underlying assets are housing mortgage loans, enterprise loans, car loans, etc.

The second model is corporate asset securitization, subject to the oversight of the China Securities Regulatory Commission (CSRC). Originators are general industrial or commercial enterprises, and the SPV used in this model is an asset-backed specific plan (ABSP) of a securities company, or subsidiary of a fund company. Corporate asset-backed securities are offered and traded on the Shanghai and Shenzhen stock exchanges. Their underlying assets come in many varieties, including accounts receivable, financial leasing claims, small loan claims and property income, as well as charge rights such as infrastructure charges, entry ticket charges, etc.

Credit asset securitization, which is based on the state-level Trust Law, is seen to have more legal certainty than ABSPs, which are based merely on administrative rules. “This explains why the CASS [credit asset securitization scheme] model has so far been the more successful model for securitizations in China,” Ong says.

A regulatory change has also helped stimulate the growth of credit asset securitization. According to Ong, credit asset securitization deals once had to be pre-approved on a case-by-case basis by the PBOC and CBRC, and sometimes clearance might not be granted due to policy reasons. For example, regulators closed the door entirely for new transactions for a number of years after the 2007-2008 global financial crisis.

However, “since April 2015, the PBOC and CBRC have implemented the registration regime – rather than a case-by-case pre-approval regime – which has greatly facilitated and encouraged the growth of CASS securitizations,” Ong says.

In addition to the two above-mentioned models, the insurance asset securitization model, subject to the oversight of the China Insurance Regulatory Commission (CIRC), has emerged in recent years. In September 2015, CIRC issued the Interim Administrative Measures for the Asset-Backed Plan Business. In late March, Taiping Life reportedly established a specific plan with underlying assets that are insurance policy pledge loans, becoming the first asset-backed securities that have insurance assets as their underlying assets.

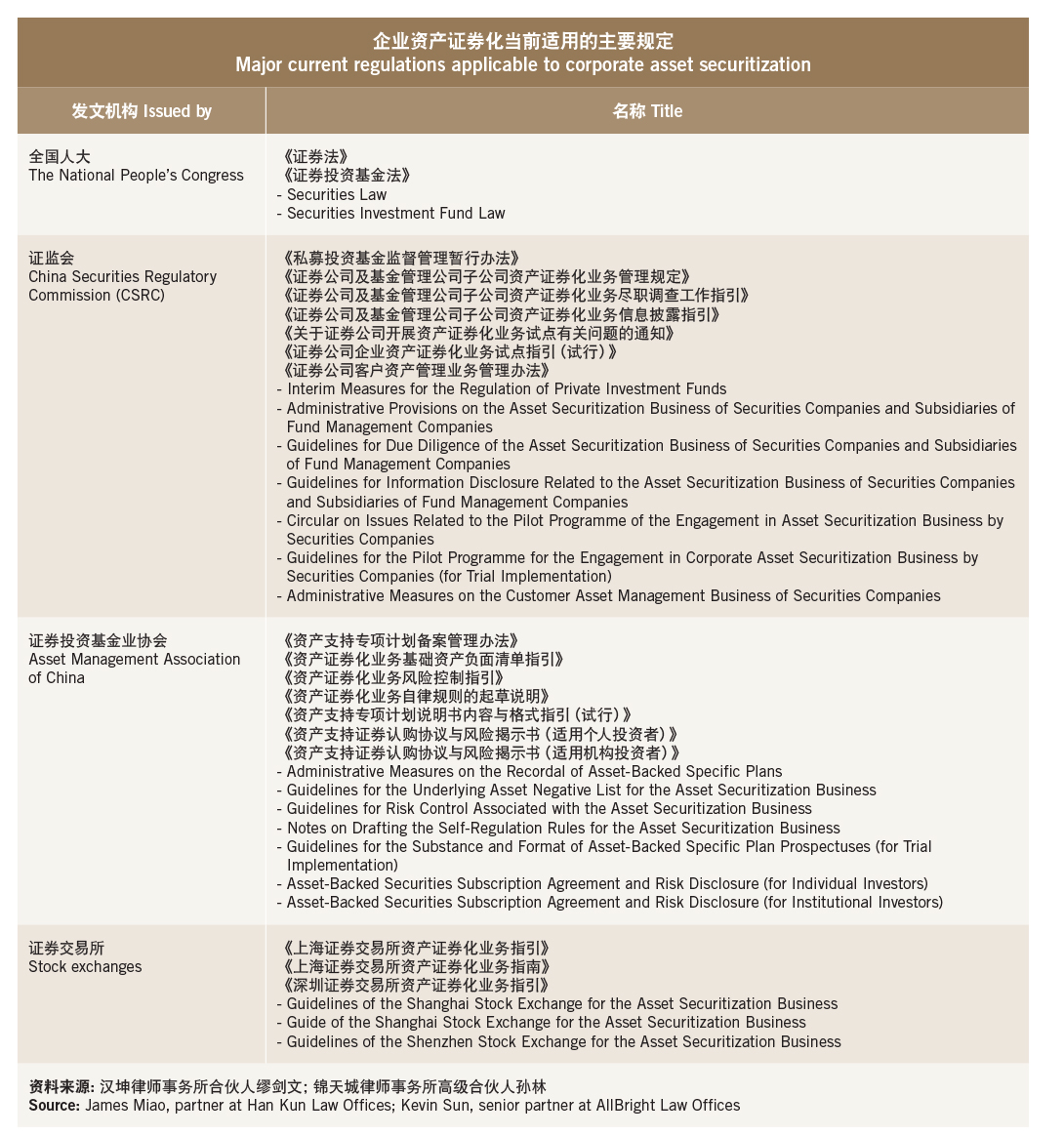

Various rules and regulations, published by a number of authorities at different levels, may be applicable to securitization transactions. The most important ones are compiled in tables on the previous two pages.

Financing alternative

A basic function of asset securitization is helping enterprises to cash in today on a cash flow that it can steadily generate in future. James Miao, a Shanghai-based partner at Han Kun Law Offices, says this can not only reduce an enterprise’s financial burden, but also makes more cash available to launch new business and investments. Taking a small-loan company as an example, “as small-loan companies have limited capital and their leverage rate for bank financing is limited, small-loan asset securitization provides a good channel, helping small-loan companies to sell quality assets to investors in exchange for cash to launch new business,” Miao says.

Compared to bank loans, the financing costs of asset securitization are relatively low – another advantage. “The most effective means of promoting asset securitization is reducing the financing costs of asset securitization through legislation and the revision of policies, motivating enterprises to seek such financing,” says Zhang Xin, a Beijing-based partner at Global Law Office.

Compared to bank loans, the financing costs of asset securitization are relatively low – another advantage. “The most effective means of promoting asset securitization is reducing the financing costs of asset securitization through legislation and the revision of policies, motivating enterprises to seek such financing,” says Zhang Xin, a Beijing-based partner at Global Law Office.

Securitization can also help diversify financing sources, providing long-term stability, Ong says. The 1997 Asian financial crisis was a lesson, which saw many businesses fold when the bank funding that they had heavily relied on dried up. “Companies that have established brands in the securitization market could turn to the debt capital markets for financing at times when their competitors are struggling,” Ong says.

Compared to financial instruments such as bonds, asset securitization emphasizes the quality of the assets, rather than the creditworthiness of the enterprise. This is conducive to widening funding channels for the large number of existing small and medium enterprises. “Many small enterprises are unable to get debt financing, or have to bear its high costs due to their limited creditworthiness conditions,” says Kevin Sun, a Shanghai-based senior partner at AllBright Law Offices. “Corporate asset securitization can help those whose ratings fail to satisfy debt issuance requirements, and those that do not even have a rating to enter capital markets to obtain financing, permitting them to rely on quality assets rather than their own creditworthiness.”

Securitization also allows large enterprises to more effectively utilize their assets. Sun says that due to the nature of the industry, some enterprises, such as heavy industry companies, will hold large quantities of illiquid assets – such as accounts payable, notes payable, etc. – for extended periods of time, while also facing large loan and bond repayment pressures. For such enterprises, “corporate asset securitization can revitalize their asset stock and enhance asset liquidity and turnover, thereby further enhancing the enterprise’s profitability”, he says.

Through asset securitization, an enterprise can remove assets of poor liquidity from its balance sheet and convert them into cash. Sun says this practice does not give rise to additional liabilities, thus allowing the enterprise to secure a new funding source without increasing its asset-to-liability ratio.

Bankruptcy remoteness

Li Yikun, the Beijing-based vice president and general counsel of Souyidai (the internet finance platform of the Sohu Group) also believes that the core of asset securitization is the transfer by the originator of the rights and interests in, and the risks associated with, the underlying assets to an SPV, thereby removing or distancing the risk of bankruptcy.

“Through asset securitization it is possible to remove the assets from the balance sheet, making it possible to reduce the company’s liability-to-asset ratio,” she says. “Removing them from the balance sheet not only impacts the debt repayment figures on the balance sheet but also the performance figures on the profit and loss statement.”

However, whether bankruptcy remoteness is achievable depends on the actual circumstances. “In some asset securitization deals, originators are required to provide security, which does not substantively change the risks to which the originator is exposed, despite the transfer of the underlying assets,” Li says. Under such a circumstance, according to the Enterprise Accounting Standards No. 23, the underlying assets do not satisfy the requirements for being removed from the balance sheet.

Drawing on the lessons learned from the 2007-2008 subprime mortgage crisis, developed markets such as the US and EU have imposed risk retention requirements on securitization originators. Credit asset-backed securities are now usually divided into several tranches, each corresponding to a different level of risk. Originators are required to hold a certain portion of the most junior tranche, the riskiest one.

China also has this requirement in its Circular on Further Expanding the Pilot Program on Credit Asset Securitization. The amount of the most junior tranche held for risk retention purposes, as mandated by the circular, should be no less than 5% of issued securities in all tranches. Current market practice is that the originator will hold the most junior tranche in order to fulfil the risk retention requirements. According to Wang Shengzhe, if the most junior tranche is too large, it will cause issues for off balance sheet transactions, since the originator still bears a large risk.

The uncertainty may also spring from the unclear timeline for establishing the trust, the SPV used in credit asset securitization. “In accordance with the market practice, the trust is established on the issue date by a public announcement. However, the subscription of the notes and signing date will [have] occurred earlier. So who is issuing the notes and signing the contracts is unclear,” Wang Shengzhe says. “As such, there may be an issue of insolvency remoteness.

“In addition, the legal opinion is not given on the issue date, when the trust is established, the assets are transferred and the notes are booked. The legal opinion is given when the originator files with the PBC for its approval to issue notes on the intro bank market, [but] at that time the transaction documents are not even signed. This is very different from the international market practice, where the legal opinions will be only issued on the issue date. This causes confusion and concern for international investors and their internal credit approvals.”

Regulatory improvement required

Stimulated by market demand, asset securitization models have become more complex. “With the continuing intensification of the current trend toward integrated development of the asset securitization business, certain new asset securitization, quasi-asset securitization and reverse asset securitization business with nested organizations or nested structures are repeatedly being seen,” Li says. She recommends that the relevant regulators jointly establish an asset securitization regulator and erect an effective regulatory regime.

From 1 May, value added tax (VAT) will completely replace business tax. Though a major reform in China’s tax regime, this may present certain problems for the credit asset securitization business. “In 2005, the Ministry of Finance and State Administration of Taxation issued a document specifically addressing the credit asset securitization business, but what it resolved were business tax-related issues; after the switch from business tax to VAT, it will cease to apply,” says Wang Jianzhao, a Beijing-based partner at FenXun Partners.

Uncertainties in the tax regime also exist for other types of securitization business. Wang Jianzhao says securitization by securities companies and subsidiaries of fund companies also faces a lack of clear, applicable tax payment rules; and for real estate investment trusts and other such immovable property asset securitization business, tax issues are one of the main obstacles to development. For a magic asset performance these may be just the trick.

Underlying assets risks

Driven by market demand, types of underlying assets used in securitization are growing more varied, drawing the attention of the market to the risks inherent in the underlying assets. “Taking specific cases as the basis to examine securitization projects, we find that the major legal issue is how enterprises select assets to package as suitable assets that can be securitized,” says Zhou Jie, a Beijing-based partner at King & Wood Mallesons.

Wang Jianzhao says that with the increasing variety in the types of underlying assets, it has sometimes become difficult to determine their legal attributes. “For example, hotel rooms, catering [and other such industries] can generate a cash flow, but how should we define the underlying assets?” he asks.

“Accepted bills are another example. Since the law currently prohibits non-financial institutions from engaging in discounting business, if securitized, how should we define the underlying assets? In practice, two different means have arisen, with one simply defining them as rights to benefit from the notes, and the other defining the underlying assets as the claims of the contracts on which the notes are based.”

Miao argues that asset securitization has already moved beyond the initial stage of a pilot project based on quality assets. “Although there is still a certain standard for the rating requirements for assets to be securitized, it is nevertheless undeniable that, with the increasing number of corporate entities involved and the weakening economy, their inherent risks have also increased,” he says. “This requires more effective credit enhancement approaches in structure design, and greater stringency in subsequent asset management.”

Risks may also come from the quality of the underlying assets, Sun says, referring to the fact that the nature of the underlying assets might affect the stability of the cash flow. The CSRC defined underlying assets that can be securitized in the Administrative Provisions for the Asset Securitization Business of Securities Companies and Subsidiaries of Fund Management Companies, but Sun says that in the end, a meticulous review by asset managers and intermediary firms – such as credit rating agencies, auditing firms and law firms – is still needed to determine whether certain underlying assets can be securitized.

In practice, Miao says some assets that do not have a fixed cash flow have been securitized by manufacturing a stable cash flow through a dual-SPV trust loan model, and warns investors of the future risks of such assets.

If an existing contract restricts new financing based on the underlying assets, or the transfer of the assets, transferability risks could arise. “Domestic enterprises’ existing financing documents, or business contracts related to underlying assets, often contain provisions restricting [asset-backed] debt issuance or underlying asset transfer, tying the hands of enterprises that would wish to securitize assets,” Zhang warns. “When signing financing documents or important business contracts, enterprises should think ahead by endeavouring to weaken or eliminate such restrictive provisions.”

Sun notes in particular the process of securitizing various types of claims and beneficial rights as underlying assets. He says there are currently no clear regulations concerning the transferability of such rights, which can expose companies to hidden legal risks. “Once a transfer of underlying assets is denied or cancelled, the entire securitization transaction framework crumbles,” he says. “Generally speaking, when transfer is prohibited by the contract, such restrictions can be resolved by amending the relevant terms. Otherwise, it is necessary to look at the beneficial rights to find out their nature.”

The validity of a transfer of underlying assets is also a point requiring attention. “In some beneficial right-related deals in which we have been involved, the generation of the beneficial rights is based on the continued operation of the originator,” Sun says. “Should the originator go bankrupt, the basis for the beneficial rights could disappear, thereby making it impossible to achieve a genuine sale.”

“Additionally, a sale of underlying assets to an SPV by the originator might fail to overcome the obstruction of the Bankruptcy Law, resulting in the court ruling that the transaction can be cancelled; or the definition about ‘real sale’ is sometimes unclear, resulting in its being found to be a transaction of another nature. In these cases, it is hard to avoid recourse by the originator’s creditors against the underlying assets.”

In addition to the above-mentioned common risks, specific assets may face different specific issues. For example, in a securitization transaction where small loans serve as the underlying assets, “to effect a valid transfer of the claims there must exist genuine transferable claims, and it is necessary to determine that the loan contracts do not contain provisions restricting the transfer of the loans to third parties; and it is necessary to notify the debtors, [failing which] such transfer will not be binding on the debtors,” Li says.

With respect to property fees and other similar underlying assets, the cash flow-back is conditional on the originator continuing to provide property services. After the sale of the underlying assets, the originator itself will continue to exist as the provider of the property services. “If the enterprise fails to provide the services at the standard specified in the contract, or commits another act that makes the forecast cash flow-back from the underlying assets unachievable, the securities holders may face the risk that the principal and interest regarding their securities cannot be repaid on time, or in full,” Zhou says.

“On the other hand, if the enterprise’s qualifications or licences to engage in business related to the underlying assets are adversely impacted by a change in regulations, an adjustment of administrative divisions or other reasons, such adverse impacts could also ultimately be transmitted to the securities holders through the specific plan. In this case, appropriate risk mitigation measures need to be put in place to ensure the interests of the investors.”

When financial leasing assets are the underlying assets, attention must first be paid to the nature of the leased items. “The nature of the leased items may make the recognition of a financial leasing relationship impossible. For example, if a highway, tunnel, water reservoir or other such immovable property or structure is the leased thing, there is a strong possibility that the relationship will instead be found to be a de factoloan relationship,” warns Lu Jingyi, a Beijing-based partner of Zhong Lun Law Firm.

When immovable property is the subject matter of a financial lease, Lu warns that for certain immovable property it is impossible to carry out registration procedure, and in this case the leased item cannot be registered under the name of the lessor, leading to unclear title to the property. Furthermore, inability of the lessor to provide the pertinent purchase contract for the immovable property, proof of acceptance and delivery, invoice and other relevant documents may also result in the failure to determine that the lessor has title to the leased item.

When the rent from the immovable property and the beneficial rights to the property serve as the underlying assets, Lu says that the failure to secure a construction project zoning permit for the relevant building will result in the invalidity of the lease contract. “Failure to secure completion acceptance recordal or fire safety acceptance recordal for the relevant building will make the validity of the lease contract uncertain and may result in the imposition of penalties by competent authorities,” he says, adding that it is also necessary to double check whether the building has been mortgaged to a third party.

There is a good chance that we will see more asset-backed securities issued by Chinese companies in future, but undoubtedly much still needs to done. For China to further expand its securitization industry, Ong gives two suggestions. One is to formulate a state-level law to provide more legal certainty for the asset-backed specific plan, and the other is to open the PRC securitization market to international investors.

Improvement in the regulatory regime will help inspire the market to conjure up more opportunities for both cash flow seekers and investors.

[/ihc-hide-content]

")