The latest reforms to India’s foreign investment regulations are significant because they tackle sensitive sectors that the government has previously been reluctant to liberalize. But concerns persist over the scope of the changes and the speed of their implementation, Ben Frumin reports from New Delhi

On a small plot in the Dwarka district of Delhi sits the hulk of an Airbus A300 jet. The plane has only one wing and hasn’t flown in years. But that doesn’t mean it’s not making its owner any money. BC Gupta, a former Indian Airlines engineer, bought it for about US$200,000 in 2003. He then sold the engines (for almost the same amount) and sawed off one wing and a significant piece of the plane’s tubular fuselage so that the remainder could fit onto his small plot.

Today, aspiring air hostesses and aeronautical engineering students train on the grounded plane. School groups visit for mock flights and simple lessons on aviation. The urban poor flock in at weekends and sit in awe, pretending they’re airborne. For most, it’s the closest they’ll ever come to a real flight.

Perhaps only in India – where there is a deluge of investment opportunities in the expanding aviation sector – could a man gross US$20,000 a month from a plane that doesn’t even fly. “It is very good money,” says Gupta with a smile.

[ihc-hide-content ihc_mb_type=”show” ihc_mb_who=”3″ ihc_mb_template=”2″ ]

The rusting, maimed airliner is an incongruous symbol of the impact of the opening of India’s economy. And that impact is set to grow following the latest round of reforms to the country’s foreign direct investment (FDI) regime that were announced on 30 January.

In a move that Jayant Bhuyan, deputy director-general of the Confederation of Indian Industry (CII), sees as a clear demonstration of the government’s will to push through economic reforms, the Cabinet Committee on Economic Affairs revealed significant liberalizations to FDI policy in a number of key sectors, not least in the burgeoning aviation industry, which the government has previously been reluctant to open to greater foreign participation.

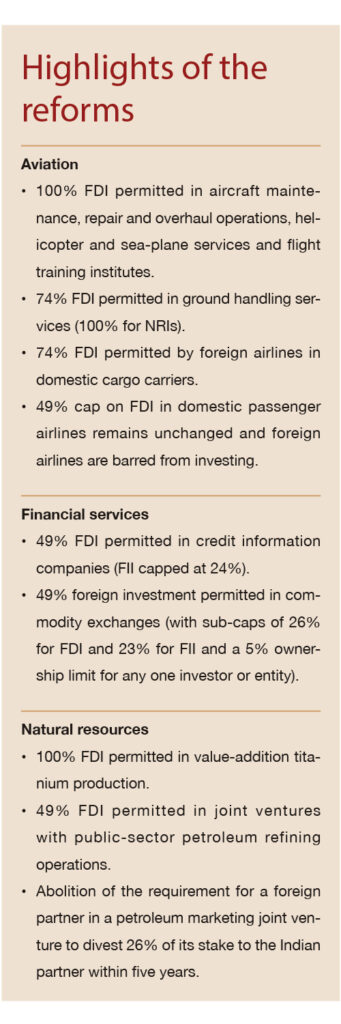

Aviation freed from old shackles

“There have been major changes in the aviation sector. FDI caps have been raised substantially in several categories,” says Dave Poddar, a partner at Australian law firm Mallesons Stephen Jaques. “Together with the ongoing measures of the government of India for privatization and/or modernization of Indian airports, these new measures could lead to the creation of international quality aviation infrastructure in India,” adds Manisha More of White & Case.

Indeed, an across-the-board FDI cap of 49% for air transport-related services has been raised in many key areas. FDI of up to 100% is now permitted by any foreign entity in the fields of aircraft maintenance, repair and overhaul operations (MRO), helicopter and sea-plane services and flight training institutes (India is suffering from a dearth of qualified pilots). Similarly, the cap on foreign investment in ground handling services has been raised to 74%, and 100% for non-resident Indians (NRIs), and foreign airlines are now permitted to own up to 74% of domestic cargo carriers. Previously, FDI of 49% was allowed in cargo airlines, but international carriers were barred from investing in these operations.

But while January’s end saw a wave of meaningful regulatory relaxations in the sector, rules regarding the biggest slice of the aviation pie – domestic passenger airlines – remain unchanged, with FDI still capped at 49% and foreign airlines barred from investing at all.

“Certain long-awaited reforms continue to remain unaddressed,” laments More.

Despite the disappointments, the new policies do present international investors with significant opportunities. “Now that FDI from foreign carriers is allowed, many major international airlines will buy stakes in Indian cargo carriers,” predicts Anirudh Mukherjee of Economic Laws Practice in Mumbai.

Mukherjee points to several in-progress MRO projects as proof of the huge foreign investment the sector is likely to see. Air India is planning four MRO facilities with Airbus and Boeing, GMR Group is working with Lufthansa Technik to set one up and Kingfisher is considering a tie-up with Gulf Aircraft Maintenance Company.

“One can see foreign companies like Menzies and SATS (Singapore Airport Terminal Services) increasing their stakes in their respective ground-handling joint ventures,” Mukherjee adds. And in capital-intensive maintenance, repair and overhaul operations – where 100% foreign investment is now allowed – many observers expect a large influx of FDI.

All of these new investment opportunities are available under the “automatic route”, which allows Indian companies to issue shares of their paid-up capital to foreigners without specific approval from the government of India or the Reserve Bank of India (RBI). Investors need only present the necessary documents and forms to a regional office of the RBI within 30 days of receipt of inward remittances and 30 days of the issue of shares to the foreign investors.

Certain sector-specific requirements, however, must still be met. For example, foreigners investing in airport ground handling services must obtain the necessary security clearances before beginning their operations. “While FDI may be possible under federal law in a particular sector, there can still be a myriad of local approvals necessary to actually implement it,” says Vishal Ahuja, a partner at Mallesons Stephen Jaques in Melbourne. “This is an important issue which needs to be considered on a project-by-project basis.”

Caps eased on natural resources

Aviation wasn’t the only industry to see liberalization in January, with several natural resources sectors also benefiting from relaxed controls on FDI.

Foreign investment of up to 100% is now permitted in titanium production, on the condition that investors add value to the raw materials they mine and guarantee to facilitate a transfer of technology.

“The changes to the titanium mining sector … will be very influential,” says Ahuja. “While the move is generally linked with the aviation industry, which uses titanium, we think the real importance is that it represents a major step in the opening up of the sensitive metals sector.”

Before the change, FDI of up to 74% was allowed in value-addition titanium production from ilmenite ore (of which India has the world’s largest known reserves). Now, the sector has been thrown open for 100% FDI, a move that Neeraj Dubey of PSA Legal in New Delhi says “will be lucrative for aircraft manufacturers like Boeing and Airbus”.

Furthermore, since foreign investors now have the option of setting up wholly owned subsidiaries, they “will no longer be required to find a suitable local partner to assist them with their Indian operations, and consequently, any possibility of management-related conflicts is completely removed,” explains Mukherjee.

But not all of the hurdles have been cleared. A plethora of sector-specific regulations such as the Mines and Minerals (Development & Regulations) Act, 1957, the Atomic Energy (Radiation Protection) Rules, 2004, and the Atomic Energy (Safe Disposal of Radioactive Wastes) Rules, 1987, have to be complied with and investors cannot take advantage of the automatic route. Instead, they must grapple with a complex approval process before the Foreign Investment Promotion Board.

In another significant change relating to natural resources, the foreign investment cap for joint ventures with public-sector partners engaged in petroleum refining has been nearly doubled, from 26% to 49%, but here too, prior approval must be sought from the Foreign Investment Promotion Board.

Bhuyan at the CII believes this change is the most important of the relaxations announced in January, and that it is “good news for international giants like Chevron, Shell and BP”. A major deterrent for investment in petroleum marketing has been the requirement for the foreign partner to divest 26% of its stake to the Indian partner within five years. “The removal of this clause will go a long way towards improving the investment environment at the front end,” says Bhuyan.

Dubey adds that “the move assumes significance against a backdrop of the interest envisaged by foreign companies such as Kuwait Petroleum in forging alliances with new refining projects of state-owned refineries,” and follows on the heels of a decision by LN Mittal to acquire a stake in HPCL refinery.

“The aim is to make India’s petroleum refining industry more internationally competitive and turn India into a trading hub for petroleum products,” explains Poddar.

New opportunities in finance

Also changed as of 30 January are investment rules for credit information companies. FDI of up to 49% is now allowed with specific prior approval from the government and regulatory clearance from the RBI. Foreign institutional investment (FII) will be permitted up to 24% in already-listed credit information companies, although it will form part of the overall foreign investment cap of 49%.

This decision “is likely to generate maximum interest among foreign investors,” says Dubey, noting that the new rules regarding credit information companies provide much-needed clarity in the sector.

Another significant relaxation is that commodity exchanges can now accept foreign investment of up to 49%, subject to sub-caps of 26% for FDI and 23% for FII. “Companies like Merrill Lynch and Goldman Sachs have been waiting to invest,” says Bhuyan. “FDI would give more depth to Indian commodity exchanges and will bring in superior technological skills to make them internationally competitive.”

An important caveat is that no single investor will be permitted to hold more than 5% of a particular exchange, and as Dubey notes, this requirement may force global players to shrink their holdings in the Multi Commodity Exchange of India and the National Commodity & Derivative Exchange. Fidelity currently owns 9% of the former while Intercontinental Exchange and Goldman Sachs together hold a 15% stake in the latter.

In addition to the relaxed investment caps on commodity exchanges, Ahuja at Mallesons Stephen Jacques points to the significance of recent amendments to the Forward Contract Regulation Act. The changes allow options and derivatives trading in commodities and give greater powers to the commodities market regulator, the Forward Markets Commission. “Greater access to derivative products is important to growth and innovation,” he explains.

Scepticism persists

But the plaudits are tempered by calls for caution as well as concern and downright scepticism.

One lawyer in Bombay says investors and legal teams alike should take the government’s announcements with a pinch of salt.

Dubey cautions that the recently announced relaxations still require an “official notification formally approving the FDI changes” as well as clarification of “the measures that [the government] will take to curb the flow of foreign funds in India”.

“These proposals are still at the proposal stage,” echoes Ketan Kothari of Thakker & Thakker in Mumbai.

Prominent local observers point to the introduction of India’s competition law, which started in 2002 but is only now beginning to manifest itself, and the long-heralded but still invisible liberalization of the legal market, as examples of delays in implementation. “Ultimately, making a decision to the press is one thing,” says Vineet Aneja of FoxMandal Little, “but that becoming law takes time.”

One reason for the delays is the fractured nature of India’s coalition government. “Maybe a lot more could have come up on the horizon had the government not been so dependent on the Left for its survival,” says Kothari.

This is particularly important considering that India will hold a national election no later than next year. “If they were to push through something that is aggressive, it might have a huge backlash when they start canvassing for votes,” Kothari adds.

Some lawyers, both Indian and international, muse that if either Congress or the BJP claims a big win in the next election, FDI rules might have a better shot at continued liberalization, particularly in politically sensitive sectors like multi-brand retail.

“If the Left is involved with any manner of the new government, I think you can forget about the laws changing in a hurry,” says Srinivas Parthasarathy, a partner at Allen & Overy in Singapore.

Yet in spite of opposition from the Left, economic liberalization continues to create opportunities for foreign investors. “Economic reform has not been completely buried in the run-up to the national elections,” Mukherjee says.

“The government’s resolve to ease the restrictions on inflows of foreign capital has come in the face of strong resistance from their coalition partners. This move provides ample evidence to support the fact that economic reforms are high on the government’s priority list.”

[/ihc-hide-content]