Legal advisers can look forward to larger and more sophisticated transactions involving Chinese investors as acquirers mature and target markets become more receptive, writes George Russell

James Hosking can tell when Chinese investment into the US skyrockets. His litigation docket fills up. Hosking, a partner with the Chaffetz Lindsey firm in New York, points to a correlation between “a wave of investor litigation over the past couple of years” and rising foreign direct investment from the mainland.

Chaffetz Lindsey has represented a number of Chinese clients in dealing with disputes related to investment in the US. “The more controversial growth area for disputes has been with the US government,” Hosking says, citing the use of US President Barack Obama’s rarely invoked executive power to block Chinese-owned Ralls Corporation’s acquisition of wind farms in the state of Oregon.

In addition, a US Congress committee recently issued a warning to American companies against doing business with Chinese telecommunications companies Huawei and ZTE. “The options for litigation to challenge these government actions are limited,” Hosking notes. “We have advised on how Chinese companies can use investment treaties to try to restrict government abuses of power.”

[ihc-hide-content ihc_mb_type=”show” ihc_mb_who=”1″ ihc_mb_template=”2″ ]

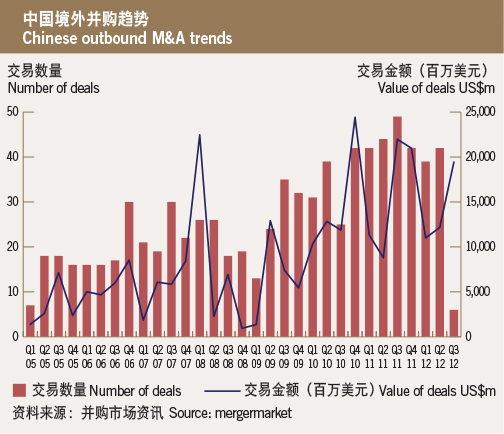

Litigators, of course, do not directly address transactional issues, but statistics back up such anecdotal evidence. According to the Ministry of Commerce (MOFCOM), Chinese investors made direct investments in 2,163 overseas enterprises in 116 territories in the first half of 2012. Total non-financial direct investment overseas amounted to US$35.42 billion, a year-on-year rise of 48.2%.

Chinese companies have been officially encouraged to invest overseas. In June, for example, 13 Chinese government departments, including the National Development and Reform Commission (NDRC), the Ministry of Foreign Affairs, the People’s Bank of China and the State Administration of Foreign Exchange issued a joint notice entitled Advice on Implementation of Encouraging and Guiding Private Enterprise to Actively Undertake Offshore Investments.

In addition, many US firms can confirm increasing numbers of transactions involving mainland corporations. “It is a good market – it’s better, deeper and broader,” says Anthony Root, a Hong Kong partner who heads the Asia corporate practice of Milbank Tweed Hadley & McCloy. Root says that despite increased scrutiny from Washington, Chinese companies remain committed to expanding their investment in the US market, which is generally viewed as a bargain.

[ihc-hide-content ihc_mb_type=”show” ihc_mb_who=”1″ ihc_mb_template=”2″ ]

One unexpected political factor that prodded them into investment in politically stable areas, adds Root, was the Arab Spring. “The Chinese lost so much money in Libya,” he says. “This, combined with the downturn and the continued weakness of developed markets, intensified their focus on the US and Europe.”

Despite the scars of 2005, when political opposition scuppered an attempt by China National Offshore Oil Corporation (CNOOC) to acquire oil major Unocal for more than US$18 billion, China resolved to re-enter the US market. “Two years ago they shed their reluctance to go into the States, although there is still sensitivity,” Root acknowledges. One Milbank client, State Grid, for example, has carefully developed its Washington relationships over the years. “They would not be shocked by the regulatory system,” Root says.

State Grid is also keen on investment elsewhere in the Americas. Last year, the power giant paid US$1.8 billion to acquire seven Brazilian transmission projects. (Milbank’s office in Sao Paulo advised the Chinese company).

Brazil is a growing destination, with Chinese investment in the first quarter of 2012 rising 118% over the same period last year. “Brazil is definitely a target country for Chinese investors due to its political and economic stability and a strong commercial relationship,” says Luis Fernando Ayres de Mello Pacheco, a partner with Veirano Advogados in Rio de Janeiro. “This trend of investment should continue.”

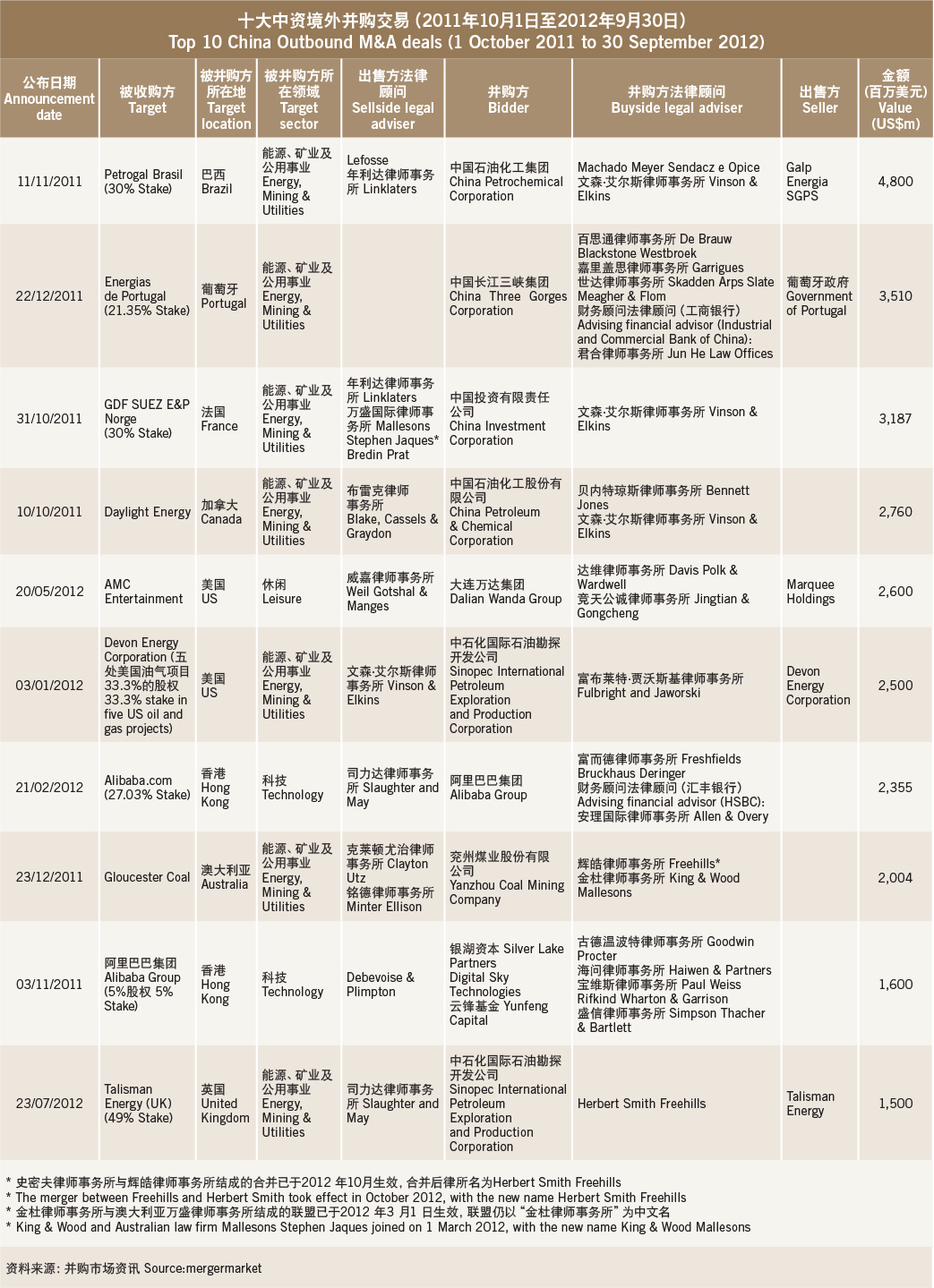

Pacheco says energy is the most attractive sector in Brazil to Chinese investors. In February, China Petroleum and Chemical Corporation (Sinopec) acquired a 30% interest in the Brazilian oil and natural gas exploration and development assets of Portuguese-owned Galp Energia for US$4.8 billion.

Linklaters and Lefosse Advogados advised Galp on the sale, the largest M&A transaction recorded by a Chinese purchaser in the past 12 months, according to data provider Mergermarket (See table on page 25). Vinson & Elkins and Machado Meyer Sendacz Opice advised Sinopec.

Vinson & Elkins was featured in another major Sinopec purchase in 2011, advising on its C$3 billion (US$2.99 billion) acquisition of Canadian oil and gas explorer Daylight Energy in the fourth-largest purchase, according to Mergermarket.

Canada is another major target for energy-hungry Chinese corporations. “The amount of investment into the Canadian energy industry, and in particular into the oil and gas industry, in 2012, could be a record or near-record year,” says Don Greenfield, a partner and co-head of the oil and gas practice at Bennett Jones in Calgary.

Canadian business circles are waiting for the marquee deal this year, which hasn’t been completed. It’s the US$15.1 billion friendly bid by CNOOC for Nexen, a Calgary-based upstream oil and gas company developing assets in Canada, the North Sea, Gulf of Mexico and off the West African coast.

Stikeman Elliott is advising CNOOC in relation to the all-cash deal, which if approved would be the largest Chinese acquisition of a Canadian company. Blake Cassels & Graydon is Canadian legal adviser to Nexen and Burnet Duckworth & Palmer is advising Nexen’s board. The Canadian government has extended its review of the transaction to 15 December.

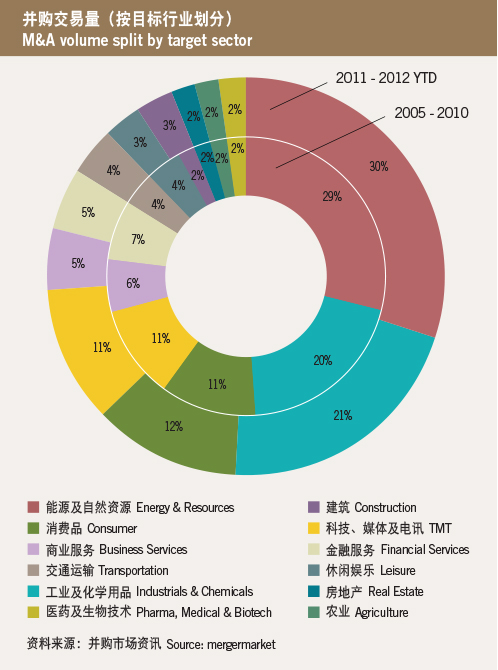

Despite the huge interest in energy – seven of the 10 largest M&A deals involving Chinese buyers were in oil and gas, and natural resources – lawyers say Chinese investment has diversified. “Two or three years ago, it was very focused on natural resources, ensuring the oil companies and the energy companies had the resources they required,” says Root at Milbank. “Since then it has evolved into a strategic outbound and financial outbound.

“It’s gone beyond natural resources into infrastructure, branded consumer products, aircraft parts and auto parts,” he adds. “They have access to liquidity and to opportunistic investments to create higher levels of return and access to technology to help move to a higher value economy.”

Chinese domestic law firms concur. “In 2009, China’s outbound investment in energy and natural resources amounted to around 80% of the total, while by this year it has decreased to near 50%,” says Zhu Ning, managing partner at Beijing firm Chance & Bridge Partners.

Zhu says her firm’s recent transactions include advising a company building a manufacturing plant in India, representing a Chinese group in its acquisition of the majority stake in an African mining company and a client entering the aeronautical sector in the US.

Just as outbound M&A activity has become more diversified, so too have the target countries. “While places like Africa, South America and Australia continue to help meet China’s insatiable thirst for energy assets, its growing interest in different types of assets is widening the geographic spread of its investments,” says David Clinch, a partner in the projects, energy, mining and infrastructure practice with Herbert Smith Freehills in Hong Kong. Clinch has advised Chinese parties on a French deal in which Shanghai Sugar Cigarette and Wine, a subsidiary of state-owned Bright Food, acquired a 70% stake in the independent Bordeaux wine merchant DIVA Bordeaux.

Lawyers see distinct categories of Chinese investors. “I see Chinese individual investors who are purchasing residential and commercial real estate, Chinese public companies looking to diversify their holdings by making strategic acquisitions abroad, and government funds or state-owned enterprises looking to acquire resources or technology overseas,” says Jason Chang, senior legal consultant at W&H Law Firm in Shanghai. Greenfield agrees that there has been diversification, but Chinese interest in Canada remains heavily energy-focused. “There has been other Chinese investment into other industries, but not on a scale approaching the investment into the oil and gas industry,” he says.

Looking towards Europe

In Europe, energy is less of an issue than bargain hunting by Chinese companies looking to expand their portfolios. However, although European assets are priced low, acquisitions are not without risks, lawyers warn. “The future development of the euro area crisis is yet unknown,” says Zhu, who advises caution.

However, there are opportunities for smart investors. “Domestic Chinese companies continue to look for ways in which to expand their global presence opportunistically, and with the debt crisis in Europe, occasions abound,” says Jean-Marc Deschandol, managing partner at Eversheds in Shanghai.

Deschandol says Eversheds has had one of its busiest years for Chinese outbound investment, with mainland clients investing in diverse targets such as British trains, Italian motor vehicles, German and Romanian solar energy and Latvian publishing.

“Outbound investment is not only increasing, but also broadening into new directions,” he says. “As a result, deals which would have been highly improbable in the past are now being successfully completed.”

This month, China Investment Corporation (CIC) announced it had purchased a 10% stake in Heathrow Airport. “We would not have envisaged such a deal being done two or three years ago,” says Deschandol. Clifford Chance advised CIC on the £450 million (US$714.5 million) purchase, while Freshfields Bruckhaus Deringer represented Ferrovial, one of the sellers.

CIC Chairman Lou Jiwei announced last year that he wanted the fund to invest in energy, water, transport and infrastructure companies in North America and Europe. Since then, it has bought stakes in the UK’s Thames Water Utilities, France’s GDF Suez and Russian miner Polyus Gold.

In Germany, Ashurst has represented a number of Chinese companies seeking assets. “Our law firm regularly advises on cross-border M&A transactions and capital raisings of Chinese companies in Germany,” says Matthias von Oppen, a partner with the firm’s Frankfurt office.

Germany poses few regulatory issues for Chinese investors outside the financial sector. “We do not see any major issues here, apart from the usual competition law constraints,” von Oppen says. “Investments in the banking sector will be challenging for Chinese investors due to the [requirement for] approval by the German Financial Supervisory Authority.”

In some cases, instead of meeting regulatory roadblocks, Chinese investors have been welcomed with incentives. Sweden has provided grants, loans and credit guarantees to inward investors from China. “We have assisted our Chinese clients with the wide range of Swedish financial incentives available to facilitate foreign investment,” says Katarina Nilsson, the resident partner in Shanghai for Stockholm-based law firm Vinge.

This year, the firm advised CECE Wind Power, a subsidiary of Zhenjiang-based CECEP Solar Energy Technology, in the acquisition of a Swedish wind power plant and Hangzhou China Century Plastic & Electronic Company in the acquisition of MW Security, a maker of secure packaging for retail stores.

Europe is not viewed as monolithic by canny Chinese investors, lawyers say. Mainland corporate raiders scour the Netherlands and Belgium for targets in agriculture, logistics and port infrastructure, for example. Germany is sought after for its technology companies, while France and Italy are obvious locations for Chinese companies seeking to acquire brands.

Southern Europe hasn’t been ignored by Chinese acquirers. “In 2012, we have filled our pipeline with deals in Spain and Portugal,” says Juan Martin Perrotto, a partner in Beijing with the Madrid-based firm Uria Menendez.

Perrotto says the diversification is a result of China’s deliberate attempt to “re-balance” its economy from one based on exports to one focused more on consumption. “The interest is strong in agribusiness, particularly wine and oil, cars, infrastructure, distribution, brands and anything that goes with technology.”

One European area that sees high Chinese interest is Belgium, the Netherlands and Luxembourg. “The acquisition of companies in the Benelux countries is promising [because] these countries, as compared with southern Europe, are affected less by the European debt crisis and companies in those countries are relatively healthy but not overpriced,” says Carola van den Bruinhorst of Loyens & Loeff in Hong Kong.

Developing new markets

Outside Europe, Chinese companies continue to concentrate on resources. “What we see happening there via the intermediary Luxembourg structures are continuing investments into resources-rich areas such as Kazakhstan, Mongolia, Australia, and east and west Africa,” says Jan Bogaert, who heads the Hong Kong office of Benelux firm Stibbe.

Some lawyers venture to suggest that the hub of Chinese investment will eventually flow away from the West to the Asia-Pacific region. “The focus of Chinese outbound investment is slowly shifting from the West to South Asia and Southeast Asia, as Chinese companies look for high-growth markets for their products,” says Santosh Pai, head of China practice at Delhi-based DH Law Associates.

Pai says investment flowing from China to India – once concentrated on natural resources – is also more diversified. “Attractive sectors for Chinese companies in India include power equipment, non-renewable energy and information technology equipment,” he says. “Engineering, procurement and construction contractors are also active, and this year a new wave of potential investors within the automotive space has also emerged.”

India, Pai adds, is emerging as a welcoming territory for Chinese companies. “Regular high-level exchanges between India and China, both through governmental and industry channels, have ensured that Chinese investments are welcomed in many sectors and regions in India.”

Still, Chinese demand for natural resources to fuel its economy appears to be undiminished. Eversheds, for example, recently advised a Chinese state-owned company on its acquisition of a mine in Indonesia.

In Australia, Brisbane firm HopgoodGanim advised Norton Gold Fields on the A$229 million (US$238.6 million) takeover bid by Jinyu (HK) International Mining Company, a subsidiary of Zijin Mining Group, China’s largest gold producer. The firm also advised Orion Metals on its takeover by Conglin International Group, a subsidiary of Huachen, a Chinese coking coal and iron ore supplier.

Chinese investors have a wide variety of interests in Australia including agribusiness, tourism, infrastructure and property. Michael Hansel, a partner at HopgoodGanim in Brisbane, Australia says investors have been heartened by new regulations easing the monetary threshold that triggers the foreign investment approval process. “These changes make Chinese ‘non-government’ investment into Australia easier,” he says.

Structuring acquisitions

Chinese clients are not only taking more active steps towards successful outbound investment – in terms of increasing the number of deals and the value of the transactions – but also undertaking more complex deal structures. “This shows us that the capability of Chinese companies to manage complex deals overseas is increasing,” says Cindy Zhao, business development director at Taylor Wessing in Beijing.

Lawyers say the unsettled global financial environment has prompted Chinese clients to look closely at foreign structures. “During the current worldwide economic recession, while seeking opportunities abroad, Chinese companies are exploring new ways and structures to control risks,” says He Jun, a partner at Concord & Partners in Beijing.

He says two new developments are being utilised. The first is that more private equity (PE) funds are involved in outbound investments. “Some of our clients are choosing to set up PE funds in Hong Kong or other jurisdictions as the outbound platform,” he says. Root, at Milbank, agrees, noting that domestic PE funds are partnering with foreign PE funds to go abroad.

The second development, says He, is a rise in the use of consortium structures. “We acted as the Chinese legal counsel to the CITIC-led consortium that purchased 15% of Companhia Brasileira de Metalurgia e Mineracao’s [CBMM] shares in 2011,” he adds. (Baker & McKenzie and Machado Meyer Sendacz Opice also advised the consortium, while Barbosa Mussnich & Aragao advised CBMM on Brazilian law).

It is unclear whether such developments constitute a trend. Zhu says her firm’s Chinese clients still mainly rely on direct subsidiaries, traditional offshore structures or variable interest entities. For his part, Perrotto believes that deals are getting simpler. “We are not seeing, for example, variable interest entities anymore,” he says. “Chinese regulators are getting smarter and very sophisticated and the global financial crisis left behind a distrust of anything that is too complex.”

Chinese investors are also looking more carefully at foreign tax structures. “When it comes down to investments in or via the Benelux, we usually implement an investment structure including a Benelux holding company,” says van den Bruinhorst, a tax partner at Loyens & Loeff. “Such holding companies enable Chinese investors to have a tax-efficient investment structure and future exit.”

Luxembourg, in particular, continues to focus on providing a stable and tax-friendly business environment, lawyers say. “Mainland entities often invest in European countries using Luxembourg holding companies,” says Stephane Karolczuk, head of the Hong Kong representative office of Luxembourg firm Arendt & Medernach.

A Luxembourg holding company – known as a sociétè à responsabilité limitée –provides Chinese investors with access to double-tax treaties, including those with China and Hong Kong. “The Luxembourg financial regulator has approved a number of renminbi products and strategies which can be implemented using Luxembourg investment vehicles,” Karolczuk adds.

Perrotto, at Uria Menendez, expects more major deals to be signed. “They will be very opportunistic, with many politically or strategically driven.” He also expects to see Chinese investors taking more minority stakes. “There are several factors that have driven this trend, we think. A non-controlling stake purchase by a Chinese state-owned enterprise in a strategic sector looks less threatening, even for the more sensible types of government.”

Lawyers warn that regulatory obstacles to Chinese investment remain across several jurisdictions. “It makes our job so interesting,” says Deschandol at Eversheds. “The US will always be challenging, in terms of its regulatory constraints and also the reception that is given to Chinese investors.”

One explanation for this is China’s own barriers to foreign acquisitions. “Given that China’s own market is not open to investment in many of the sectors that Chinese companies are investing in overseas, the lack of reciprocity may encourage resistance towards Chinese investors,” he says.

What foreign investors won’t see often are bids from privately owned Chinese companies. “I think the private domestic investors are very much focused on the Chinese domestic market,” says Root, who expects CIC, the sovereign wealth fund, to make more direct investments, but still not taking majority positions.

Suspicion over the level of government involvement will also continue to raise flags, Deschandol adds. “With many Chinese companies being state-owned, or financially backed by the Chinese government, they are not arm’s length investors. This presents both legal and political issues for their foreign counterparts.”

[/ihc-hide-content]

")