China is striving to achieve a new balance between traditional and renewable resources. Richard Li does some digging for the relevant legal and business concerns

The beginnings of a change of tack that may be of epic proportions is showing an increasing influence over China’s mining and energy needs. An insatiable appetite for coal and oil has always held sway, needed to feed the industrial maw of manufacturing from the raw materials that Chinese mining giants have extracted from pits and shafts around the world.

The end product of all this activity has left a nation choking under pollution. “For the scarcity of fossil fuels and the consequent environmental pollution, China is rapidly developing renewable/clean energy with a series of favourable policies, in the hope that its current resource consumption dominated by traditional resources can be transferred as early as possible to be dominated by renewable/clean energy,” says Wang Jihong, the executive partner at Grandway Law Offices in Beijing.

Changes in policy are none too soon and this sea change is producing a new desire to lead global competition in renewable energy technologies. Interests in solar and wind technology are being pursued with particular zeal. But will this trend last? And what about the future of traditional mining and energy interests?

[ihc-hide-content ihc_mb_type=”show” ihc_mb_who=”1″ ihc_mb_template=”2″ ]

Sustainable development demands that China reform its structure of resources consumption – and the country is doing so. China aims in its 12th Five Year Plan for Renewable Energy to generate 11.4% of total primary energy from non-fossil sources by 2015, and 15% by 2020.

The country’s craving for developing renewable resources may also be driven by the external environment. In the traditional resources sector overseas, China faces competition with Western countries and major Asian economies like India, Japan and South Korea. Some target countries have focused more on restricting foreign involvement in resources projects. The development of renewables can help reduce China’s reliance on these traditional resources.

Environmental concern is another reason. Most of China’s policy activities in this industry are about the control of carbon emissions, says James Douglass, a Beijing partner at Linklaters. “So by the cumulative effect of all these policies the Chinese economy is being propelled along a lower carbon path.”

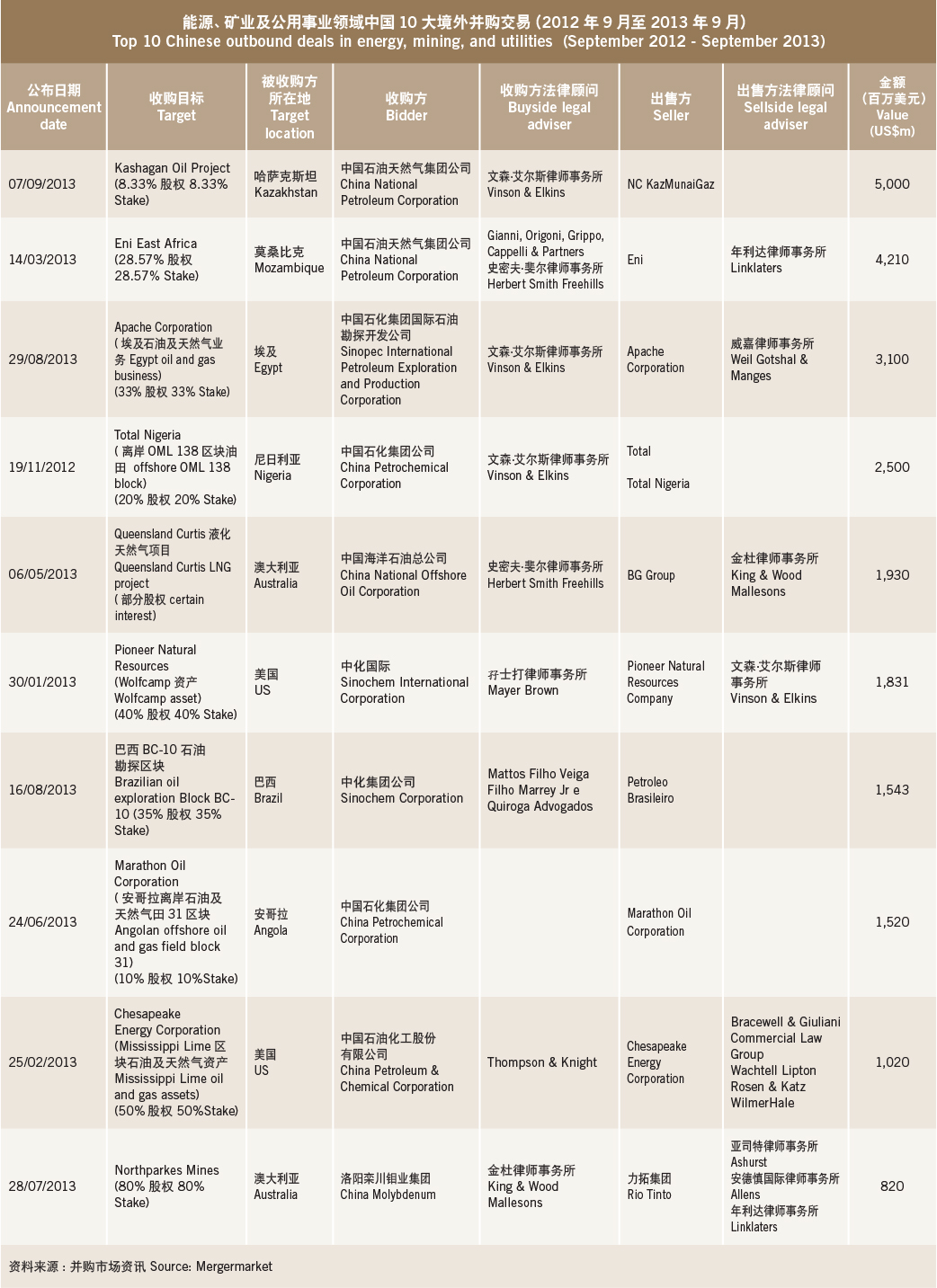

However, for the time being China’s fast growing economic engine still relies on traditional resources. In late August, for example, Sinopec agreed to pay US$3.1 billion for a 33% stake in Apache Corporation’s oil and gas business in troubled Egypt.

Trends for traditional resources

Still, China is not keen to play with fire. “China tends to invest more in countries with political stability and mature legal frameworks [such as Australia and Canada],” says Xu Ling, a Beijing partner at Guantao Law Firm. In countries like Syria, Sudan and Libya, due to volatile political situations, Chinese investment develops at a slower rate.

“Owing to the significant cultural and legal differences between China and Latin American countries, Chinese outbound investment hasn’t grown too much,” Xu observes, also noting that with the further development of the China-ASEAN free trade area, Chinese investment is increasing fast in Southeast Asian countries like Cambodia, Indonesia, Malaysia, Thailand and Vietnam.

In the upstream oil and gas sector, Chinese state-owned oil companies are acquiring assets “on a truly global scale … and across the full range of opportunities from conventional oil and gas and LNG to unconventional gas, mostly shale”, Douglass says.

“Much of the focus has been on acquiring reserves or by securing supply, usually through financing by Chinese banks of foreign reserve holders,” he says, “but quite a bit of this activity is focused on securing technology or expertise.” In the mining sector the situation is much the same, he notes.

For foreign investors in China, Paul Deemer, a Beijing partner at Vinson & Elkins, thinks a key recent legal change is the elimination of the requirement for the Ministry of Commerce (MOFCOM) to approve oil, natural gas and coal-bed methane contracts, and amendments of such contracts, with foreign parties under the regulations on Sino-foreign co-operative exploitation of offshore or onshore petroleum resources. “The elimination … reduces uncertainty for oil and gas investments in China and shortens the time required for entering into or amending such contracts,” he says.

But still, Xu notes that mergers and acquisitions (M&A) by foreign investors in the traditional resources sector have decreased. “It’s mainly because China tends to tighten its regulation of foreign investors’ inbound acquisitions, and the prices of mineral and energy products are falling,” she says.

And there are other options, for example nuclear energy.Wang Jihong thinks nuclear power will become the major non-fossil energy in the future, adding that “[China] has the largest nuclear power capacity under construction around the globe”.

New energy opportunities

Contrary to the traditional sector, foreign investment in new energy sectors is being encouraged. Xu says the Foreign Investment Industry Guidance Catalogue encourages foreign investors to help develop the industrial chain and technologies in solar energy, wind power, biomass energy, etc. “Foreign invested high-tech companies in new energy sectors also enjoy tax incentives,” she adds.

According to Wang Weidong, the managing partner at Grandall Law Firm in Beijing, the State Council published a decision in mid-May to delegate its power of administrative approval for more than 100 items, among which are projects utilising hydropower, thermal and wind power. “China has also eliminated the limitation on the percentage of foreign parties’ participation in clean-energy power generation equipment,” Deemer says.

However, Wang Weidong sounds a note of warning on investing in China’s clean energy industry. For example, despite the rapid development of wind power in China in recent years, “the overall profit margin is still relatively low and the investment payback period is much longer”.

Transportation is another hurdle. “China’s resources are unevenly distributed,” Wang Weidong observes. “Wind power and solar power resources are concentrated in the northwest, which means that the resources centre and the transportation load centre are reversely distributed.”

The global market potential for renewable energy is also tempting China to increase its investment overseas. “Within the last 10 years, China has invested in 33 nations around the world in solar and wind energy companies,” says Xiong Jin, a Beijing partner at King & Wood Mallesons (KWM). Antonio Vicente Marques, the founding partner of AVM Advogados in Luanda, observes that “most of the Chinese investments were in developed countries”.

Xiong says in developed regions like North America and Europe, “many countries have implemented policies to attract domestic and foreign investments”. For example, Germany has feed-in tariffs, and the US has tax credits and loan guarantees. China’s investment in the developed regions is also driven by “the possibility to obtain cutting edge technology and know-how”, he adds.

Xu at Guantao says developed countries have a large demand for clean energy like wind and solar power. “And as a result of the financial crisis, opportunities are available in these countries for cheap acquisitions of their quality assets,” she says.

In 2012, China’s largest wind turbine manufacturer, Titan Wind Energy, announced its acquisition of Vestas’ turbine manufacturing plant in Denmark. “[To Titan], Europe offers the most promising outlook for offshore wind energy,” Xiong says.

Early this year, KWM advised Guohua Energy Investment on its acquisition of a 75 % stake in Hydro Tasmania’s Musselroe windfarm project. “Upon completion, the total installed wind power capacity of Guohua in Australia will exceed 300 megawatts,” Xiong says.

China is also very active in the field of solar energy. “China is one of the world’s biggest solar plant manufacturers,” Xiong says, adding that Chinese company Trina Solar recently won the deal of supplying 1.1 million solar panels for a power plant in the desert of Nevada, US.

Chinese companies are also very interested in investing overseas. China Solar Power Holdings recently acquired two US solar panel companies – a 100% stake in ThinSilicon, and a 51% stake in Terra Solar Global.

“European solar energy companies are [on] the radar of Chinese companies as well,” Xiong continues. Chinese company LDK Solar acquired a 33% and 38% stake of German company Sunways respectively in 2012. It provides “China’s second-largest solar-panel maker access to new technology and a distribution network in the world’s biggest photovoltaics market,” he says.

In Africa, China’s investment in renewable energy is also booming. “This is largely due to governments’ efforts to open up their economies for private investment and the possibility of feed-in tariffs,” Xiong says, adding that for this reason, Chinese companies Yingli Solar and Suntech Power have invested in solar plants, while Goldwind and Guodian Longyuan have preferred to invest in windfarm projects in South Africa.

However, trade disputes can hamper Chinese renewable companies. “In the European Union, it is being discussed whether Chinese solar panels have been sold below market price in order to gain market share and put European companies out of business,” Xiong warns.

The US is also alert to this price issue. The Obama administration shields domestic companies from Chinese competition by imposing tariffs on Chinese solar panels.

But US policy is not only building barriers on price – or on solar technology. Last year, Chinese-owned Ralls Corporation in the US was denied access to buy a windfarm near a navy area in Oregon. “National safety was cited as the reason for rejection,” Xiong says.

Solar panel manufacturers in Europe and the US also grumble about China’s prices. Recently German companies Conergy and Gehrlicher Solar filed for insolvency reportedly due to China flooding the market with cheap panels. American companies Solyndra and Abound Solar are also reported to blame subsidised Chinese panels for dragging down prices.

Chinese companies may be keen to acquire competitors that are financially weak. “The acquisition of a competitor is one of the means to obtain its technology and expertise,” says Philipp Melcher, a lawyer at Gleiss Lutz in Brussels. “Such an acquisition is often possible at more attractive commercial terms when the target competitor is in difficulties.”

Ulrich Soltesz, a Brussels partner at Gleiss Lutz, says “while there have been recent examples of struggling European and US manufacturers being acquired by Chinese competitors, others have tied up with non-Chinese competitors, so there seems to be a general trend in the market towards consolidation.”

Given China’s current reliance on traditional resources, and the development of renewable energy, some important regions are worth being examined further in detail.

Australia

Allens has seen a recent slowdown in Chinese investment in Australia’s traditional resources sector. “This is not to say that investment has stopped, it is just not occurring with such frequency,” says Kate Axup, a Beijing partner at the firm. “Chinese investors are certainly looking at assets, but making considered judgements.” Hilary Lau, a Hong Kong partner at Herbert Smith Freehills, says Chinese investors are “exercising more caution and deliberation in execution with much more due diligence and verification undertaken”.

On the regulatory front, the newly elected government has caused some uncertainties for the foreign investment review process. Martin Klapper, a partner at HopgoodGanim’s Brisbane office, says the new government has proposed to reduce the threshold that triggers examination by the Foreign Investment Review Board from A$248 million (US$232 million) to A$15 million. “The reduction in this threshold could have the potential to stymie, or delay, lower to mid-level investments that were previously not captured,” he says.

But the tax regime may become more favourable. One policy of the new government is “to repeal both the carbon tax and the mineral resource rent tax”, Klapper says, but this may take some time to come true.

Geoff Simpson, a Perth partner at Allen & Overy, says Chinese investment in Australia’s renewables sector is “fairly buoyant”. “There are strong renewables resources in Australia,” he says, “and the market is buoyant as a result of the [favourable] regulatory regime.”

Herbert Smith Freehills has seen lots of Chinese investment in windfarms in Australia. “Primarily, they seem to be investing directly in the windfarms as a means of deploying their technology and gaining some credibility from [financiers] and [financier] confidence in their technology,” says Stuart Barrymore, a Perth partner at the firm.

Alex Ding, a Sydney partner at Allens, says for Chinese investors in Australia’s wind and solar energy industry “the attractions are that they can make an appropriate return on their investments here, compared to the returns in China”.

A main challenge, Barrymore says, is securing long-term power purchase agreements (PPAs). “This is a problem common to all investors in renewables in Australia at the moment.” Another problem, says Simpson: “The change of government and the uncertainty with respect to the regulatory framework.”

“Australia has traditionally supported the continued development of cheaper fossil fuels, at the expense of renewable energy,” Klapper says, adding that the new government plans to scrap the Clean Energy Finance Corporation, which provides loans to renewable energy companies.

In terms of competition confronting Chinese investors, Simpson says Indian investors remain interested in coal and some other commodities, and Japanese investors in Australia’s main export earners – coal, iron ore and liquefied natural gas (LNG). Chinese companies are competitive due to their access to finance, Ding says. “But in terms of improvements, Chinese investors often need to show a strong degree of commercial management style, i.e. they are real businesses operating in order to make a profit.”

Brazil

Rodrigo do Val Ferreira, the chief representative at Felsberg e Associados in Shanghai, says that particularly due to Brazil’s restrictions on direct foreign investment in natural resources, in recent years foreign investment in mineral and energy resources has decreased, although oil investment may be an exception. Paulo Vieira, the founding partner of Vieira Rezende in Rio de Janeiro, says Chinese oil companies such as Sinochem and Sinopec have already partnered with major players in Brazil, “and CNOOC is prospecting new opportunities in the market”.

The Mining Code is also under the spotlight. The Brazilian government recently submitted to its National Congress a bill that if passed “would rewrite the current Mining Code”, says Guilherme Vieira, a partner at Tauil & Chequer in association with Mayer Brown in Rio de Janeiro. “The most significant [change] is the new procedure for granting mining titles, which would be through public biddings, as it already occurs in the oil and gas industry.”

Ferreira adds that, according to the current draft, “there should be no restriction” for foreign investment in mineral resources. “However, the fact that there is still no definite version of the law still causes uncertainty for investors in this area”, he warns.

Francisco Rohan, a partner at Tauil & Chequer in association with Mayer Brown in Rio de Janeiro, says Chinese companies will find a very competitive mining sector in Brazil, “since all major mining players worldwide have a presence in the country”.

Glenn Faass, the managing partner at Norton Rose Fulbright in Bogota, has been representing mining and energy clients in Latin America. He says China is a recent arrival in Brazil compared to countries that have decades, “or in some cases a century” of prior investment history. “Those countries, including the US, Canada and European countries, and their national champions, have a significant head start,” he says.

But things change. “[Nowadays] even Latin American countries with strong relationships with the US and Europe want to diversify investment sources and customers,” Faass says. This may bring opportunities to other investors like China.

Pedro Aguiar de Freitas, the managing partner at Veirano in Rio de Janeiro, particularly points out Indian companies as obvious competitors to Chinese investments. “[But] Chinese investment capacity is what makes Chinese companies competitive in the Brazilian mineral and energy business,” he says.

Paulo Vieira warns Chinese investors against “the complex legal system of Brazil”. “Brazilian red-tape laws are still considered a challenge for investment in the country,” adds Freitas, despite recent efforts on tax and labour issues.

Ferreira thinks Chinese companies should be more prepared to understand a different legal and political framework, and cultural differences. “Japanese, American and European companies are still ahead of Chinese companies in understanding and adapting to different environments, and localising their management skills,” he says.

Paulo Vieira says there seem to be more Chinese companies providing equipment for Brazil’s renewable energy industry, but a big hurdle for equipment exporters to the country is the local content rules, which will soon become mandatory for the electricity sector. “Investors should consider joint ventures with local partners or direct investment in local facilities in order to add some degree of local content to their products,” he says.

Canada

The Investment Canada Act has seen recent changes that may cause uncertainty for foreign investors. One revision is that [foreign] state-owned enterprises (SOEs) are not permitted to acquire control of Canadian oil sands businesses, except in exceptional circumstances, according to Donald Greenfield, head of the oil and gas practice at Bennett Jones in Calgary. “[But] no guidance is given as to what those exceptional circumstances would be,” he adds.

Greenfield says the act was amended in June this year so that the Canadian government has the power to determine that SOEs have acquired control of Canadian businesses “even though their acquisitions may not have passed the ‘bright line’ control thresholds in the act”. The June revision has added uncertainty. “For example, this determination could be made where a joint venture agreement gives an investor control over material decisions even though it has a minority ownership interest,” Greenfield says. “However, no guidance has been given by the federal government as to how these new rules will be applied.”

Canada may be an attractive destination for clean/renewable energy investment. “The Canadian government supports the industry through favourable tax treatments for research and development, and the establishment of two funds aimed at funding the development and demonstration of innovative technological solutions in clean technology,” says Stephen Wortley, the Hong Kong office chair of McMillan.

But Wortley warns that the clean/renewable industry in Canada is an evolving sector, and companies face a broad range of legal issues including environmental law, aboriginal matters and employment law.

Some of the legal issues can affect investment in traditional mineral and energy resources as well. “The environmental assessment process in Canada is more rigorous than in China,” says Sandy Wang, a Vancouver partner at McMillan. “In most cases, major resource projects must obtain approval from both federal and provincial governments, and generally speaking the review will take 18 months to several years or more.”

Labour deployment is another concern. Robin Junger, a Vancouver partner at McMillan, says Canada lacks a skilled workforce for the many energy and mining projects. “But bringing in temporary foreign workers is a sensitive matter … federal laws have recently been changed to impose certain new requirements,” he adds.

Kazakhstan

Aliya Zhumabek, a senior associate at Colibri Kazakhstan in Almaty, says Kazakhstan remains attractive for Chinese investment into traditional mineral or energy resources. “Also it is worth noting that, in addition to investments in primary industry, both states are interested in launching projects in process industry as well,” Zhumabek says.

However, it might be a problem to get consents from government authorities for acquiring subsurface (or subsoil) use assets. The investment process is neither simple nor quick, says Joel Benjamin, the managing partner at Kinstellar in Almaty, especially for Chinese investors. “There have been fewer deals closed because of the perceived high concentration of Chinese investment, often resulting in delays in obtaining, or even refusals to grant, the necessary consents,” Benjamin says.

The Kazakh law on subsoil use is subject to frequent amendment, but the next amendment draft may bring good news. “Presumably, for the first time in recent years these amendments would be aimed at investment climate improvement,” says Natalya Braynina, an Almaty partner at Aequitas Law Firm.

Kazakhstan has seen many Western investors, mainly from the US and Europe, withdraw from the country’s energy and oil projects, says Olga Chentsova, the managing partner at Aequitas in Almaty. “The main reasons stated by investors are excessive state regulation of the oil industry, the absence of long-term guarantees, and also delays in the start-up phase of projects,” she says.

Against this background, it is not improbable that Kazakhstan will continue to follow a policy of attracting Chinese investments, Chentsova says, adding that the number of companies with Chinese capital is now increasing in Kazakhstan’s oil sector. One example may be CNPC’s US$5 billion acquisition of an 8.33% participation interest in the Kashagan project from KazMunaiGas.

Anvar Ikramov, a Tashkent partner at Ashur Law Firm, says the financial crisis of 2008 helped increase China’s influence in the region. “Now, huge financial potential of the Chinese economy and large investments into economies of those [Central Asian] countries, as well as into the economy of Kazakhstan, makes China a major player in the region,” he says.

However, Nurlan Sholanov, also an Almaty partner at Aequitas, says people in Kazakhstan are “psychologically afraid of Chinese expansion, which, against the background of the known fact of the low quality of Chinese consumer goods, gives rise to the criticism of [state] policy favouring Chinese investment”.

Resistance to using local workers may also trigger discontent. “Despite requirements under Kazakhstan law to use local content – local providers of goods and services and local employees – Chinese companies often prefer to use Chinese employees and contractors,” says Adlet Yerkinbayev, an Almaty partner at Kinstellar. Yerkinbayev warns that the legal regime for hiring foreign employees has been tightening in Kazakhstan.

In the renewable energy sector, Zhumabek has seen some co-operation memorandums executed between Kazakhstan and China. “The government pays particular attention to development of this field of economy and seeks investors for such development.” But she warns foreign investors against “the law’s imperfection and gaps … since the clean or renewable energy industry is a recently developing industry [in Kazakhstan]”.

Africa

The South African Department of Energy promulgated a plan in 2011 aiming to generate 17,800 megawatts of new electricity from renewable sources in the next 20 years, according to Greg Nott, a director at Werksmans Attorneys in Johannesburg.

Rita Chen, an associate also in the firm’s Johannesburg office, says under the independent power producer procurement programme, the Department of Energy began in 2011 inviting interested parties to submit proposals for the finance, construction, operation and maintenance of renewable energy generation facilities. Given the eagerness of the participants, “there is every reason for optimism about the next two phases”, she says, in which the original target of 3,725 megawatts for bidding is expected to be increased by the Department of Energy. In the traditional resources sector, Nott has seen Indian, Korean, Japanese and European companies competing alongside Chinese investors. He says that it’s important for Chinese investors to overcome the dominant perceptions that “Chinese construction, while fast, does not compete at the same level, as far as quality is concerned, as its international competitors”.

Nott highlights a deal towards the end of 2012, in which a China-led consortium acquired a 74.5% stake in Palabora Mining Company from Rio Tinto and Anglo American. “This mining transaction is indicative of continued Chinese interest in South Africa’s resources and indeed the continents,” he says.

In Nigeria, China’s business involvement in Nigeria’s mineral and energy resources has risen significantly in the past decade, says Fehintola Sofola, an associate at FO Akinrele & Co in Lagos.

Sofola says the Petroleum Industry Bill 2012 (PIB) is under debate in the Nigerian legislature. “If the current version of the PIB is passed into law, it will lead to drastic changes in the industry,” she says. “It aims to make the Nigerian oil and gas industry more transparent, productive and attractive to foreign investment.”

It is a positive signal to the industry that the PIB 2012 provides that licences and leases shall be granted only after an “open, transparent and competitive bidding process conducted by the inspectorate”, Sofola continues. “The bill does not discriminate between international oil companies, independents and indigenous companies, in terms of applicable tax rates.”

According to Sofola, in order to build local capacity and expertise Nigeria introduced restrictions on foreign involvement in its oil sector in its 2010 Oil and Gas Industry Content Development Act.

Angola has seen “considerable” Chinese investment since 2004 in the oil and gas industry, says Marques at AVM Advogados. “But it has been pointed out that Chinese oil companies have yet to develop the technology required to exploit deep and ultra-deep water oil resources, and this has been seen as one of the main difficulties Chinese oil companies are facing in Angola,” he observes.

“Foreign investors in the oil and gas sector should bear in mind that the government will continue to look for the increase of transfer of skills and technology, training of Angolan nationals and outsourcing to Angolan companies.”

Uganda sees increasing Chinese investment into traditional resources, says Jamina Apio, an associate at Shonubi Musoke & Co Advocates in Kampala. For example, she says Sinohydro Group has gained the contract to build Karuma hydro project, which is Uganda’s largest electricity plant on the River Nile.

Apio says China is active in the clean and renewable energy industry in Uganda. “Uganda is an agricultural country with vast fields of fertile land, with the production of crops such as sorghum, rice, maize, etc., which are perfect for biomass fuel and other renewable energy production.”

It’s worth waiting to see how China’s growing appetite for renewable resources may influence the global market, and whether it will spur the development of new legal frameworks for renewable/clean energy in countries where the industry is emerging. How China manages its own transition from a major consumer of traditional resources to a frontier clean energy user is also a major consideration in this multibillion-dollar sector.

[/ihc-hide-content]

")