The imminent introduction of India’s new takeover code presents an opportunity for regulatory arbitrage

The acquisition of shares of a listed company in India is currently governed by the Securities and Exchange Board of India (Substantial Acquisition of Shares & Takeovers) Regulations, 1997. In September 2009, the Securities and Exchange Board of India (SEBI) set up the Takeover Regulations Advisory Committee (TRAC), which was given the mandate of realigning the regulations so as to “catch up” with developments and ensure they reflect globally accepted best practices.

The TRAC, in its report submitted to SEBI in July 2010, recommended a comprehensive overhaul of the existing framework and has put together a set of draft regulations.

With a change of guard at SEBI (CB Bhave stood down as SEBI’s chairman on 17 February and has been replaced by UK Sinha) and a regulatory change in the offing, there is a rare opportunity for companies to take advantage of a period of regulatory arbitrage.

[ihc-hide-content ihc_mb_type=”show” ihc_mb_who=”3″ ihc_mb_template=”2″ ]

During this time, they may choose to enjoy the benefits of the 1997 regulations or structure commercially advantageous transactions under the new TRAC regulations that are pending notification.

Acquiring new targets

For open offers, the 1997 regulations mandate a minimum offer size of 20%. The TRAC regulations, however, mandate a 100% offer size. Companies looking to acquire a 51% shareholding in a listed target company may benefit from launching their offers prior to the notification of the TRAC regulations while it is still possible to obtain 51% control without making an offer for 100% of the target.

However, if the commercial objective is to consolidate a target company entirely, the TRAC regulations offer a 0–100% acquisition model. Shares of the target company will be automatically delisted if the post-offer shareholding of the acquirer is more than 90% and the acquirer has stated its intention to delist upfront. No separate delisting offer will be required under the SEBI Delisting Regulations, 2009.

Indirect acquisitions

An international company that is looking to acquire an international target with an Indian listed subsidiary as an insignificant asset would probably choose to effect its control under the 1997 regulations. In so doing, it will make use of the “chain principle” that was recommended by the Bhagwati Committee Report, 1997, and declared law by the Supreme Court in Technip SA v SMS Holding (P) Limited.

Under the chain principle, a company that acquires a controlling interest in another company and indirectly acquires shares in a subsidiary of that company as a result, may not be required to make an open offer for the subsidiary. However, an offer would be necessary if the intermediate company’s shareholding in the subsidiary amounted to a substantial part of its total assets or if the purchaser’s primary objective for acquiring the intermediate company was to gain control of the subsidiary.

Under the TRAC regulations, there is no scope for the application of the chain principle. Therefore, all indirect acquisitions that give the acquirer control over an Indian listed company, or enable it to exercise voting rights in excess of a certain level, will trigger a mandatory open offer.

The TRAC regulations distinguish between indirect acquisitions that are disguised as direct acquisitions and genuine indirect acquisitions. For instance, if the genuine target is a “predominant part of the business” of the entity being acquired, such an indirect acquisition will be treated as a direct acquisition for all purposes (price, timing of the public announcement, etc.) under the TRAC regime.

An underlying Indian-listed company will be deemed a “predominant part of the business” if the net asset value, sales turnover and/or market capitalization of the underlying company represents more than 80% of the net asset value, sales turnover and/or deal value of the primary acquisition target.

If the Indian-listed subsidiary is deemed not to be a “predominant part of the business”, the TRAC regulations offer some price protection. In such cases, the offer price is to be calculated with reference to the date of the primary acquisition, even though the public announcement for the Indian company is made later.

Schemes of arrangement

Acquisition structures involving schemes of arrangement that result in the substantial acquisition of shares or control of an Indian listed company will be subject to some additional requirements under the TRAC regulations.

Under the existing regulations, a scheme of arrangement under any law, with or without court approval, is exempted from mandatory open offer obligations, with no pre- or post-transfer SEBI reporting requirements. But under the TRAC regulations, an acquisition that is made according to a scheme of arrangement will be exempt only if it is approved by a court or a competent Indian or foreign authority.

In cases where the scheme of arrangement does not involve the listed company directly as the transferor or transferee company, additional criteria will need to be satisfied. These include conditions that the component of cash and cash equivalents in the consideration should be less than 25% of the total consideration and that the entities that directly or indirectly hold at least 33% of the voting rights in the target company are the same as those that held the entire voting rights before the implementation of the scheme.

Non-compete payments

A key driver in the price negotiations for acquiring a potential target is the payment of a differential consideration to exiting controlling shareholders. This is currently paid under the 25% “non-compete” component permitted under the 1997 regulations.

Under the TRAC regime, all payments made to the seller under any “incidental, contemporaneous or collateral agreement” will have to be attributed to the offer price. However, this may not be a valid reason for launching an acquisition under the 1997 regulations as opposed to the TRAC regime since for the last four years SEBI has generally resisted the payment of non-compete considerations to exiting shareholders.

Consolidation of holdings

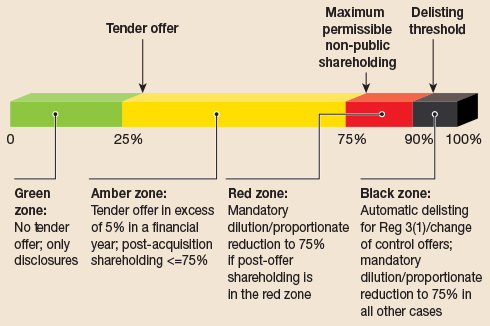

The triggers and “creeping acquisition” limits under the TRAC regulations are described in the diagram below:

Under the TRAC regulations, financial investors – especially strategic investors who are yet to make up their mind on taking over a company – may acquire up to 24.9% of a listed company without triggering mandatory tender offer obligations. This raises some concerns for promoters (significant shareholders who are often the company’s founders) as “shadow control” may be exercised by predators who have acquired just under 25% of the shares. In practice, such predators may be able to exercise significant voting rights as a result of the “multiplier effect” caused by absenteeism in general meetings.

The 1997 regulations set this trigger point at 15% and the change may pose a challenge to shareholders who hold more than 15%, but less than 25%, of the shares. Such shareholders may now wish to increase their holding to more than 25% before the TRAC regulations take effect.

If they do not, crossing the 25% threshold at a later date will mandate a 100% tender offer, which may be outside their funding capabilities.

Creeping acquisitions

The TRAC regulations contain a widely worded “repeal and savings clause” that is intended to safeguard any rights that companies had accrued under the 1997 regulations. It may be argued that the creeping acquisition right afforded by the 1997 regime represents one such “accrued right”. However, a better case may be made if an investment decision towards such accrued rights (such as through the acquisition of warrants or other convertible instruments) has already been made.

Shareholders who own more than 55% of a listed company will no doubt welcome the extension of the creeping acquisition limit to 75%. This change has come about as a result of TRAC rejecting the concept of “greater control”. Under the 1997 regulations, the acquisition of a single share or voting right by a shareholder who already holds between 55 and 75% of the shares triggers a mandatory tender offer. Such shareholders are currently permitted to only make a one-time creeping acquisition of 5% through secondary market purchases on the normal segment of the stock exchanges or through a buyback. Under the TRAC rules, they will also be able to increase their shareholdings by way of preferential allotments of 5% per financial year at a fixed determinate price.

Furthermore, once the TRAC rules take effect, shareholders who hold more than 25% will be eligible to make smaller voluntary offers for target companies of a minimum size of 10% (instead of the currently mandated 20% offer size), subject to their post-offer shareholding not exceeding 75%.

Hostile acquisitions

The TRAC regulations seek to create a simplified procedure for competitive bids, while also plugging some of the loopholes found in the 1997 regulations.

For example, the new rules require a committee of independent directors to provide reasoned recommendations on an open offer to the shareholders of the target company. This has the potential to introduce the Revlon rule into Indian takeover jurisprudence. The rule was formulated in the Delaware Supreme Court decision of Revlon Inc v MacAndrews & Forbes Holdings Inc. It requires the directors of a target company to be proactive in identifying and pursuing the best deal for their shareholders. A superior competitive offer would, therefore, be expected to receive a favourable recommendation by the target company’s directors.

Furthermore, while competing offers are being considered, the target company will not be able to appoint additional directors to its board (except in the event of death or incapacitation of an existing director). This measure is designed to ensure that the interests of competing bidders are protected.

In contrast, the current regulations effectively require target companies to go into “freeze and desist” mode. There have also been several recent cases in which the interests of hostile bidders may have been compromised as a result of target companies appointing new board members who were connected with one of the competing bidders.

A clean and clear exit strategy for the losing bidder is facilitated by the TRAC regulations. Subject to the 75% threshold, the successful acquirer may acquire the shares of competing acquirers in an open offer within 21 days of the expiry of the offer period without triggering another open offer.

Funds and financing

Triggering a mandatory tender offer obligation requires the acquirer to put in place “firm financial arrangements” with respect to the entire amount payable in the offer. The 100% offer size required by the TRAC regulations effectively compels the acquirer to raise funds equalling the entire market capitalization of the target company prior to making an offer (irrespective of how much they may actually acquire). In addition, to complete the underlying transaction and to appoint directors to the board of the target company in the period before the transaction is finalized, the acquirer must deposit the entire amount in cash into an Indian escrow account (a non-interest bearing account for foreign acquirers).

Given the prohibition on financial assistance by target companies and the limitations on acquisition financing by banks, an Indian acquirer may find it difficult to finance a takeover under the TRAC regime. While there is no certainty that the Reserve Bank of India will relax its rules to assist Indian acquirers, some respite has been suggested by the TRAC in its detailed provisions on non-cash consideration.

Such non-cash payment options also exist under the 1997 regulations, but have seldom been used. This is because of the regulatory difficulties thrown up by the SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2009, which effectively treat such stock for stock transactions as “public issues” under Indian securities laws.

Recent transactions have therefore seen interesting combinations of strategic and private equity funding to bridge the gap between the non-availability of bank finance and the strategic dreams of high-growth entrepreneurs. Such cross-over private investment in public equity transactions is expected to increase under the TRAC regime.

Invoking withdrawal rights

Under the 1997 regulations, the withdrawal of an open offer is only permissible if regulatory approvals are not granted. There have been instances where SEBI has compelled acquirers to complete open offers even though the underlying trigger transactions have been rescinded.

The TRAC seeks to pass on some of the risk of deal failure to public shareholders in the event that an underlying transaction should fail for reasons outside the control of the acquirer.

High-risk targets may therefore be pursued under the TRAC regime with greater comfort coming from the knowledge it is possible to withdraw from a contract – and the mandatory open offer – in the event of the discovery of fraud or another material adverse change.

Internal restructuring

The TRAC regulations will considerably reduce the number of inter se transfer exemptions that are currently available under the 1997 regulations. Transfers will be possible only between immediate relatives, persons named as promoters in the shareholding pattern of the company for not less than three years and persons under common control (those with less than 50% equity holding).

The wide range of transfers that have been undertaken under the “group” exemption or the “collective transferee or transferor” exemption will not be permissible under the TRAC regime. Parties seeking to make transfers under these exemptions are advised to do so now before the TRAC regulations are notified.

The 1997 regulations provide a blanket exemption to shares acquired through a rights issue by promoters. This is subject to there being no change of control and irrespective of the voting threshold that was crossed. The TRAC regulations, however, will exempt such acquisitions only by shareholders who are already above the 25% mark.

Corporate actions such as buybacks, which result in an inadvertent increase in the voting rights of the promoters, will now be eligible for an automatic exemption as long as there is no change of control and the acquirer abstains from voting in the special resolution of the shareholders that authorized the buyback.

[/ihc-hide-content]

Cyril Shroff is a managing partner of Amarchand & Mangaldas & Suresh A Shroff & Co. Amita Choudary is a principal associate.