To some foreign investors, exiting India in the current climate may seem like a wise move. But finding a way out may be harder than staying put

Foreign investors could be forgiven for viewing their business struggles in India as a sign of karmic retribution. The threat to enforce retroactive tax provisions, unfulfilled promises of sectoral liberalization and the ghost of Vodafone – spectres that appear to defy all logic – continue to haunt corporate barons, like a shadow of bad deeds from the past.

Add to this a sunken economy trapped in a policy gridlock and you can quickly envision a bleak picture of an investor on crutches trying desperately to navigate the thicket of regulations and laws for commercial gain.

It may seem depressing. But just how hazardous is the situation for foreign businesses in India? Are international investors worried without reason? Views differ.

“Nothing much has changed fundamentally in India’s economy or ecosystem in the last five to 10 years,” says Vijay Sambamurthi, the managing partner at Lexygen in Bangalore. “The one factor that has changed is the perception of the regulatory system.”

Some say that investors will readily face security risks in dangerous jurisdictions, but are unwilling to contend with political fracas and a weak legal system.

Splinters in the system have forced many investors to reconsider their positions in India. Some that were exploring new transactions have put their plans on hold; others are rolling back their operations to cut losses while they still can. Many with businesses in highly regulated sectors have run out of patience, having believed for years the government’s assurances that further liberalization was imminent.

“More than 10 years have gone by since insurance was first liberalized and we’re still standing at 26%,” notes Seema Jhingan, a partner at LexCounsel in New Delhi. “Talks to increase the foreign investment cap even to 27% are leading to heated debates.”

Foreign retailers, disillusioned by the reversal of a decision to lift investment caps on multi-brand retail, are also losing their appetites for expansion. UK retailer Tesco called the deferment “a missed opportunity for Indian producers, farmers and consumers”.

Telecom companies from overseas, too, are assessing their options. Having lost money and business opportunities as a result of the Supreme Court’s licence cancellations, some are negotiating exits, while others contemplate new strategies. Foreign investors, even outside of the sector, are monitoring developments with trepidation.

“The Supreme Court is trying to redress the situation caused by the larger corruption scam,” says Sambamurthi. “But if you put yourself in the shoes of a foreign company, the question is, at what point in time are we really safe? Will we find out after investing billions of dollars that there’s something fundamentally wrong with our transactions?”

[ihc-hide-content ihc_mb_type=”show” ihc_mb_who=”3″ ihc_mb_template=”2″ ]

Why leave?

Policy paralysis and regulatory riddles may be good reasons to exit but they are seldom cited as the main ones. Over the past 18 months, India has seen exits from Sara Lee, Thomas Cook, Bulgari, New York Life Insurance, Etisalat, Gazprom and Fidelity Asset Management, to name a few. All gave different reasons for their decision.

New York Life said it needed to focus on its North American business; Bulgari moved out after disappointing results; and Fidelity fled after continued losses.

For Sara Lee and Thomas Cook, withdrawing from India was part of an effort to reduce debt, strengthen balance sheets and focus on core businesses. “The exit was done to monetize the asset and not linked to the regulatory environment in India,” says Harsh Pais, a partner at Trilegal who advised Thomas Cook on the sale of its Indian arm.

Russia’s Gazprom put an end to its 50-50 production-sharing contract in the Bay of Bengal with GAIL, India’s state-owned natural gas distribution and processing company, after drilling three exploratory wells that failed to reveal commercial gas reserves.

Trigger events

In most cases, exit rights are negotiated at the time of the entry agreement. A large part of early negotiation is devoted to a discussion of these rights to ensure that any potential departure process is a seamless and painless one. Private equity funds, for example, will state categorically before an agreement is executed what events will trigger an exit from the investment.

In a franchise agreement, trigger events for an exit could include violations of intellectual property rights, a misuse of the franchisor’s brand and concept, failure to reach a particular milestone, creating a sub-franchise, a lack of transparency in the accumulation and calculation of royalties, and the non-payment of royalties.

But an agreement can be violated in countless different ways, so it is impossible to stipulate every material breach that could potentially occur. Instead, the clause “any other material breach of the terms and condition of this agreement” is used to cover non-compliance that cannot be predefined or pinpointed.

Earlier this year, a US-based franchise chain in India ended its relationship with a franchisee when the latter exceeded the per outlet budget authorized for the setup of around six outlets in India and generated revenues that were far lower than expected, reducing the royalty payouts.

“Most of the breaches that I’ve seen revolve around non-compliance with certain agreed milestones, market penetration, expansion targets and conformities with the agreement, leading to a deficit in relationship and mistrust which causes an exit,” says Jhingan. She adds that non-payment issues and/or depressed royalty or franchise fee payouts (which are based on revenues) are a frequent driving factor for breakups of licensing, franchising or technical collaborations.

Licensees and franchisees usually accept most of the terms and conditions set out by the licensor or franchisor in order to have access to established business concepts or know-how. In joint venture collaborations, the mechanics of an exit may differ because the parties have better bargaining power and both negotiate hard to get to the agreement stage. “The exit clauses are more detailed and there’s a lot more give and take and negotiation prior to execution and closing of the deal,” says Jhingan. “Exit clauses here relate much more to the failure of the parties to contribute to the growth of the collaboration in a manner outlined in the agreement, or perform their agreed obligations and compliances which may include capital infusion to the business.”

Which way out?

The standard exit options for a foreign investor in an unlisted Indian company are through an initial public offering, a put option on an Indian promoter, a swap of shares of the Indian unlisted company with a listed company of the same group, or an amalgamation of an unlisted company in which a foreign investor has made an investment, with a listed company of the same group.

The IPO route is popular as it entails finding a fair value, creating a market for the stock and usually making a profit. However, with the current volatility in the capital markets, the IPO route may not be realistic.

“You typically give a company three to four years to IPO,” says Gunjan Shah, a partner at Amarchand Mangaldas in New Delhi. “But as things stand, we don’t know where the markets will be four years from now, we don’t know whether the company will be able to IPO or not. So everyone keeps it as an option in the docks, but there’s no guarantee it will happen.”

Over the past year and a half, the Reserve Bank of India (RBI) has raised objections to the use of put and call options. It believes that an equity investment made by a foreign investor backed by a put option at a pre-agreed internal rate of return does not amount to an equity investment, or a foreign direct investment, but is rather a debt investment. This is because it is a guaranteed exit at a guaranteed price, which the RBI says equates to an external commercial borrowing. “So put options are not on the table anymore,” says Shah.

Investors could opt for a share swap or the amalgamation process, but Shah warns that no route offers a guaranteed exit and none can be characterized as speedy. “Exits will always take time,” she says. “Of course, if a foreign investor wants an exit at the end of year four, we start the process at the beginning of that year. We provide for the necessary filings, applications and other actions to be taken way in advance, but other than that, there’s not much you can do.”

Distorted valuations

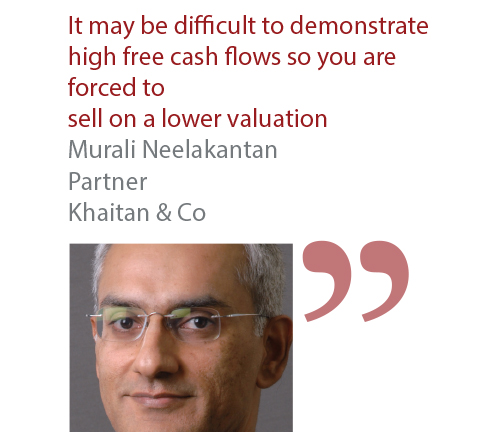

The process of selling shares to exit may be fairly simple, but the requirement to value the shares on a forward discounted cash flow (DCF) basis has created a huge problem for foreign investors. Before this method was introduced, investors could choose whatever valuation methodology was appropriate. Murali Neelakantan, a partner at Khaitan & Co who worked on Bahrain Telecommunications’ exit from India, says the DCF system is based on a series of assumptions and encourages investors to fabricate information that could lead to a higher valuation.

“If you have an asset-heavy company, then DCF may undervalue your company,” says Neelakantan. “As the foreign party who is the seller, you could say ‘I have a lot of real estate, factories, etc.’ It may be difficult to demonstrate high free cash flows so you are forced to sell on a lower valuation … They can’t just revalue their assets which have already been valued in their balance sheets. It’s a system that works in a skewed way.”

To avoid the pricing conundrum, Neelakantan suggests setting up a joint venture offshore, perhaps in Singapore or Mauritius, with a subsidiary in India. This, he says, will effectively ship not only the pricing systems overseas, but also any disputes that could occur, which could mean quicker enforcement than if the agreement was drawn up in India.

Sambamurthi says investors who have relied on jurisdictions such as Mauritius should keep a close eye on developments in relation to the Direct Tax Code (DTC) and general anti-avoidance rules (GAAR) in India. “The DTC’s introduction has been delayed to next year, so in that sense, there is perhaps a window now to get M&A deals done to exit positions held in Indian companies,” he says, but cautions against exiting primarily on the basis of tax considerations.

Finance minister P Chidambaram has already announced his intent to review the retroactive applicability of GAAR and certain aspects of the DTC proposed by former finance minister Pranab Mukherjee. “Developments like these are welcome and will help boost investor sentiment,” says Sambamurthi, “but it is important to monitor implementation closely.”

The problem with going private

Taking a public company private once an investor has exited can be tricky. Since amendments made in 2010 to the Securities Contracts (Regulation) Rules, 1957, any company listing its securities on an Indian stock exchange is required to have a public float of at least 25%. Listed companies that had a public float of less than 25% when the amendment came into force must raise their public shareholding by a minimum of 5% every year until it reaches 25%. Listed companies that fall below the 25% public float must raise the float to 25% within 12 months.

Thomas Cook sold its 77% stake in Thomas Cook (India) to Fairbridge Capital (Mauritius), a subsidiary of Toronto-based Fairfax Financial Holdings, through an auction process. Fairbridge made an open offer under the provisions of the Securities and Exchange Board of India (Substantial Acquisition of Shares and Takeovers) Regulations, 2011, to acquire the remaining equity shares from public shareholders after executing the sale agreement. But if Fairfax wanted to delist and take the company private, it would have to wait a year from the completion of the offer before making a voluntary delisting offer. During that year, it would have to reduce its stake to 75%.

It was unclear under India’s previous takeover regulations whether an acquirer could begin the delisting process without first selling down its stake within the one-year period.

“This is an issue that’s quite controversial,” says Pais. “There is no justification for making it so difficult to take company private because it’s bad for both the seller and buyer. The seller finds it difficult to exit their position and the buyer for the same reason has to jump through more hoops and possibly live with the publicly listed company when they would prefer a privately held company.”

A long winding road

Foreign investors with subsidiaries in India should be prepared to be patient when planning their exits from India. A client of Aliff Fazelbhoy, a senior partner at ALMT Legal in Mumbai, obtained a licence to set up a merchant banking and stock broking unit. However, the client then decided to exit before the unit was in full operation due to financial constraints.

The exit process required the client to: (a) deregister with the RBI as a non-banking financial company; (b) surrender its registrations with the Securities and Exchange Board of India; and (c) appoint an individual as a voluntary liquidator and complete the winding up process under the Companies Act, 1956, including filings with the official liquidator and the registrar of companies. Fazelbhoy estimates this entire process could take approximately 12-16 months to complete.

Sambamurthi has a client who has been trying to wind up its Indian entity for four years. The delay is due to ongoing service tax litigation with the Indian government. According to Sambamurthi, the amounts in question are not high, but this is holding up proceedings.

Labour labyrinth

Foreign investors with manufacturing subsidiaries could find themselves shackled by India’s stringent employment law provisions. The country’s labour laws provide detailed procedures that must be followed when shutting down an industrial establishment. This could include compensation for workers being laid off and perhaps offering them positions elsewhere if this is a viable option.

“You need a legally workable action plan,” Sambamurthi says. “If there is a union, you need to make sure you get their buy-in both in principle and in writing.” He adds, however, that foreign investors should be wary of workers taking advantage. “I have seen companies encounter less trouble upon exit when they pay attention to labour issues and come up with generous settlements where they look after their employees. But workers can still be unreasonable despite this … make sure you are extremely fair and transparent, but at the same time, make sure workers don’t take advantage of you.”

Sticky situations

Under an oil and gas production sharing contract (PSC), once a decision to exit has been made, issues between the various companies comprising the contractor as well as between the contractor and government need to be dealt with. Issues between the contractors themselves could include addressing outstanding cash calls, general and administrative expenses, audits, etc. The government and contractors meanwhile may need to sort out practical issues such as PSC audits, physical well abandonment approvals, repatriation of funds, etc. Routine administration such as closing their joint account and disposing of inventories also need to be addressed.

Environmental compliance is, of course, a significant aspect of the exit process. A contractor is required to perform all necessary site restoration, which includes proper abandonment of wells, removal of equipment, structures and debris, establishment of compatible contours and drainage, replacement of top soil, re-vegetation, slope stabilization, in-filling of excavations and taking all other action necessary to prevent hazards to human life or to the property of others or the environment. The contractor is required to prepare a proposal to restore the site including an abandonment plan and submit it for the consideration and approval of the management committee. It is crucial that this is done properly because the contractor may be held responsible for any environmental damage or problems caused by its actions in the future, even if the exit is complete.

Sumanto Basu, a partner at J Sagar Associates, highlights another stumbling block for investors in the hydrocarbons sector, relating to bank guarantees. Most investors exit during the exploration phase, which lasts seven to eight years, depending on which new exploration licensing policy (NELP) round agreement they have signed. Some investors will ask for an extension of the phase for six months or a year. Certain extensions require the submission of a bank guarantee.

“Those bank guarantees sometimes don’t get put in and the government allows the extension without making an issue out of it” says Basu. “But when you’re exiting, all the paperwork needs to be perfect – so if you find oil or gas, it’s fantastic. And then a lot of things are forgotten and you move on to the development stage.” He notes however, that when there is no find, and you need to close your accounts, the government is much stricter. “They know that if it’s a foreign operator and they are allowed to leave, they will ultimately remit whatever money is lying in their bank account and go away.”

Communication and evidence

Lawyers encourage investors to hold regular meetings to monitor progress and ensure dialogue between the Indian and foreign parties involved. The lawyers know that cracks in a business relationship that are not addressed early on can surface at the time of a split. Jhingan is currently handling two termination matters going for arbitration and explains that in both cases, the foreign party seems to have multiple grievances against its franchisees/licensees, not one of which has ever been raised or documented in a written communication. “How do we prove all the concerns our client had for the last two years?” she asks.

Investors may ignore things that could support them at a stage when a joint venture or franchise agreement may sour, and seek to avoid conflicts and complaints at all costs in a bid to strengthen and sometimes salvage relationships that are on the verge of collapse. Still, Jhingan suggests mapping of agreed milestones from time to time, regular updates and reports or meetings followed by signed minutes of the meeting, which can help “build up a case of compliances” and aid in identifying which party is in the wrong to achieve a beneficial settlement on exit.

She also advises investors to include mediation as an option under negotiated exit routes to “ease friction and create a harmonious situation”.

[/ihc-hide-content]

Taking off

Christopher Holschier, deputy press spokesman at Fraport explains why the company has decided to leave India

It is important to differentiate between Fraport AG’s two areas of activity in India: (1) our 10% share in the DIAL Delhi International Airport Private Limited consortium that operates and develops Delhi airport; (2) our representative sales office which covers India (and occasionally some other parts of Asia).

With regard to our participation in DIAL: Fraport has held a 10% stake in the consortium since 2006, when Delhi International Airport was privatized. The other shareholders include GMR Group (an Indian company involved in infrastructure development for the road transportation and energy sectors) with 54%; Malaysian Airports Holding with 10% (via a subsidiary company); and the remaining 26% is controlled by the state-owned Airports Authority of India, which has a blocking share. DIAL’s 30-year concession for operating and developing Delhi’s international aviation gateway commenced in May 2006.

Furthermore, as the designated “qualified airport operator” in DIAL, Fraport is required to fulfil the function of airport (lead) operator at Delhi Airport for at least seven years. This period expires during the first six months of 2013. Thus, we have made a strategic evaluation of our participation in DIAL.

All of the major construction projects have been completed (such as an interim terminal, “landside” links, vehicle parking facilities, runway system, and the new landmark international passenger Terminal 3 that serves as India’s aviation gateway to the world.

With these major projects completed, our 10% share clearly gives us only a minority position to play – and serving merely as a passive financial investor over the long term would not meet our international strategy.

This is why we have undertaken discussions with the other DIAL partners and the state authorities about our intention to divest our stake by the time the seven-year period expires in the first half of 2013. Independent of this divestiture, if requested, Fraport could continue to offer know-how to Delhi Airport.

In terms of our branch office, this one-person (German) representative office was tasked with sales and business development activities in India, occasionally in other Asian countries, too. Given the current situation in India, we do not see any further airport privatization potential on the horizon. This is why we are closing the office.

Nevertheless, we fundamentally consider India to be a very interesting market and, as such, we are keeping an eye on future projects in India, which is still very much on our radar. We are very proud of the successes achieved with DIAL in making Delhi a vital and modern aviation gateway for the benefit of India and of international travellers around the globe.