Careful business decisions and tightened purse strings have changed the pace and direction of Indian outbound investment

At a time when the global markets continue to be muted and domestic activity is curtailed by slowing growth and a governance crisis, India Inc is treading gingerly in the international arena. Indian companies are still shopping globally, albeit cautiously.

“It’s a good time to buy companies abroad as they are not overvalued,” says Seema Jhingan, a partner at LexCounsel in New Delhi. Even so, Indian companies are in no hurry to match the frenetic deal making of the Chinese. Today, many are driven mainly by business decisions rather than the desire to acquire random assets in the global discount sale.

Earlier, India’s outbound investments were fuelled by a booming stock market and easily accessible financing. Present day M&A transactions, by contrast, are a by-product of business requirements and affordability, a natural fallout of the global economic downturn.

“People have money but they are not willing to make big bets anymore,” says HV Harish, a partner in the India leadership team at the Bangalore office of Grant Thornton. “Earlier companies went overseas with a boom mentality, but now with overleveraged companies there is uncertainty about India itself and they want to evaluate every buy.”

[ihc-hide-content ihc_mb_type=”show” ihc_mb_who=”3″ ihc_mb_template=”2″ ]

This pragmatism has made corporate India conservative. “It’s a tight situation,” says Jhingan. “Our economy is not in the pink of health and companies want to save on pennies.” Reserve Bank of India (RBI) data show that Indian companies spent US$27.29 billion on outbound investments in the 12 months to 31 July 2012. Between 1 April and 31 July 2012, India invested US$9.8 billion in global assets compared to US$13.2 billion in the same four months last year. “The seriousness of Indian buyers has improved in the last few years,” says Jhingan. “Experimentation is not for most clients but consolidation is.”

Corporate cautiousness was evident in the nine months from 1 April to 31 December 2011. Outbound investments dived 28.3% to US$25.25 billion from US$35.23 billion in the same period of the previous year, according to RBI data. Investments by Indian companies in 2011 slid 16.2% to US$33.89 billion from US$40.45 billion in 2010.

The large multibillion-dollar deals of just a few years ago – like Tata Motors driving away with Ford Motors’ iconic British brands Jaguar and Land Rover in 2008, Tata Steel snapping up British steel giant Corus in 2007, and Bharti Airtel buying the sub-Saharan assets of Kuwait’s Zain Telecom in 2010 – have given way to modest acquisitions.

The ticket size of investments now generally ranges from US$25 million to US$350 million. “Investments have shrunk but the basket of deals is more with mid-sized acquisitions in different sectors,” explains Shardul Thacker, a partner at Mulla & Mulla & Craigie Blunt & Caroe in Mumbai.

The scale down is an outcome of both domestic and international pressure. Also, in the past year the Indian rupee has spiralled downwards – depreciating 21% against the US dollar to currently trade at ₹55.6 levels.

“The outbound investment scenario is not as active as before,” says Amrish Shah, a partner and transaction tax leader at Ernst & Young in Mumbai. “Investors have [to factor in] the news emanating out of the Eurozone, presidential elections in the US and grapple with the financial crisis.”

Resource rush

Natural resources are an urgent concern – a quarter of India’s 1.2 billion population has no access to electricity; there is a power deficit of 8-12% during peak hours with outages running for over eight hours. India needs to almost double its current generation capacity from 170,000 megawatts to 330,000 megawatts in the next decade.

On 31 July, 600 million people in India – nearly one in 10 people in the world – suffered power cuts in what was possibly the world’s largest electrical failure in history. Smelling huge opportunity, almost every big and small corporate house has diversified into the power sector in the past few years with hydro, thermal and coal interests.

Data from deal tracker Dealogic show that in the 12 months to August, Australia has been a favourite haunt for Indian companies. They have been purchasing coal mines for power plants back home, where there is a shortage of the raw material. India needs over 670 million tonnes of coal this year, but is expected to produce only 554 million tonnes, for a shortfall of 116 million tonnes. By 2017, the country’s requirement is expected to reach 1 billion tonnes with a shortfall of 300 million tonnes.

One of the most aggressive players in this sector is GVK Power & Infrastructure. In the second half of last year, GVK acquired a 79% stake in the Alpha Coal and Alpha West projects, and a 100% stake in Hancock Coal’s Kevin’s Corner project in Queensland, Australia. GVK group vice-chairman Sanjay Reddy, who has relocated to Australia, is racing to complete the land acquisition to put up the rail corridor for the US$10 billion Alpha Coal Project.

Raffle prize

Indian companies are raising their game with new investments in Asia’s Lion City

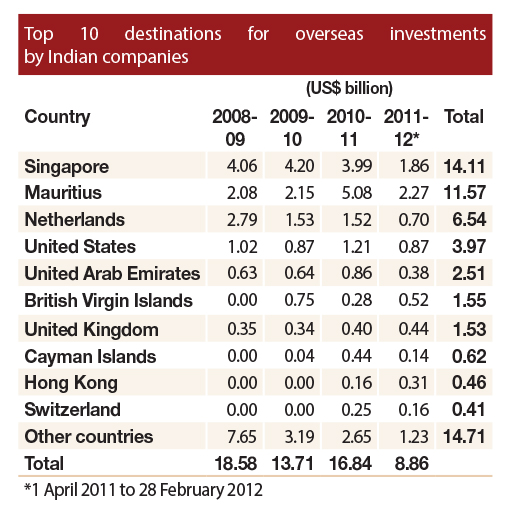

Singapore was the most sought after destination for India’s outbound investment from 1 April 2008 to 28 February 2012, garnering US$14.11 billion, Reserve Bank of India (RBI) figures show (see table).

Singapore, like many of its rivals, has a double taxation avoidance agreement with India. With the right infrastructure to manage investments and an encouraging regulatory milieu, the Lion City has attracted many companies and affluent Indian entrepreneurs over the years. Tata Steel invested US$96.79 million via a subsidiary in financial services, insurance and real estate in Singapore, the RBI said.

Many law firms in Singapore have their plates full with Indian clients. Indian companies have not only invested in the city, but are using it as a stepping stone to penetrate other markets. “There has been a trend for most of the Indian companies to set up a holding company in Singapore for either raising funds for their offshore projects, or making investments into coal assets, iron ore or other natural resources in and around Southeast Asia like Indonesia, Malaysia, Myanmar, Hong Kong, China and Australia,” says Manik Verma, a Singapore-based consultant in Watson Farley & Williams’ Asia practice.

Many law firms in Singapore have their plates full with Indian clients. Indian companies have not only invested in the city, but are using it as a stepping stone to penetrate other markets. “There has been a trend for most of the Indian companies to set up a holding company in Singapore for either raising funds for their offshore projects, or making investments into coal assets, iron ore or other natural resources in and around Southeast Asia like Indonesia, Malaysia, Myanmar, Hong Kong, China and Australia,” says Manik Verma, a Singapore-based consultant in Watson Farley & Williams’ Asia practice.

Companies are increasingly receiving external commercial borrowings and offshore loans for investments in assets such as ships, coal, other minerals, oil and gas blocks and aircraft, he says.

Some companies may not even have a business in the region. Yang Yen-Thaw, a foreign lawyer and co-head of the India practice at Dacheng Wong Alliance, says, “Many Indian companies are also taking proactive steps to set up a presence in anticipation of conducting business from and through Singapore.” Yang has seen Indian interest in neighbouring countries such as Indonesia, Malaysia, Thailand and Vietnam. Indian clients have also shown interest in Singapore’s hospitality sector.

“India has faced a challenging year domestically, impacting the value of the rupee,” says Low Kah Keong, co-head of WongPartnership’s India practice and head of the firm’s asset management and funds practice in Singapore. “The currency’s resulting weakness has affected corporates keen on overseas acquisitions. Yet the less than favourable environment has also been an incentive for Indian businesses to look elsewhere to invest.”

_

GVK acquired a 100% stake in the rail line and a 60 million tonne per year port as part of the pit-to-port solution, according to the Press Trust of India. The combined projects will create one of the largest coal mining operations in the world, the company says.

Increasingly, companies are looking for more control of logistics to help shield them from the potential volatility of coal prices. Moreover, “By taking equity positions in foreign coal mines, they get access to the imported coal that they need at the cost of production, rather than at the current coal price from time to time,” explains Philip Catania, a partner at Australian law firm Corrs Chambers Westgarth. “Even if these companies don’t actually take physical delivery of their equity share of coal, their ownership interest acts as a hedge against price movements.”

Canada – a popular target for Chinese investment in the energy sector – has been wooing Indian companies. India’s state-run Oil and Natural Gas Corporation is in the process of wrapping up an overdue deal to buy a piece of Conoco Phillips’ share in the Alberta oil sands for around C$5 billion (US$5.1 billion).

Indian trade and M&A with Canada was C$8 billion in 2011. “The activity levels are not high but there are high levels of expectations and goodwill, and we are targeting C$15 billion by 2015,” says Richard Balfour, a partner and national practice group leader at McCarthy Tétrault in Toronto.

India and Canada are currently negotiating a free trade agreement and finalizing a bilateral investment treaty. “These agreements will provide Indian and Canadian companies with remedies to address trade or investment barriers or problems encountered in each country,” says Balfour.

Canada also provides access to Africa, which adds to Canada’s attractiveness, Balfour says: “Many companies are based in Canada but own mines in Africa.” For instance, in July, Jindal Steel and Power acquired Canadian miner CIC Energy, which holds 6 billion tonnes of high-grade thermal coal in Botswana, for C$116 million.

Hasty play and financial storms

Lawyers are unanimous in their belief that the buying price and the ability to manage an asset are equally critical. “Any acquisition needs to be strategic – it has to add value to the acquirer in different ways rather than solely expansion, although that too can be a value add from the purchase,” says Prashant Mara, consultant and co-chair of Osborne Clarke’s India group in London.

The purchase by Hyderabad-based Dr Reddy’s Laboratories of German generics player Betapharm in 2008 illustrates how overlooking purchase price may hurt an investor in the long term. The Indian pharmaceutical company had revenues of US$540 million and paid US$600 million for Betapharm. The expensive acquisition was a drag on the company for the subsequent two or three years.

The rationale for acquiring Betapharm was simple: Have cash, so buy. Satish Reddy, Dr Reddy’s managing director and chief operating officer, is candid on the company’s website: “It didn’t fit into any perfect strategy plan – something came up at that time so we went after it,” he admits.

In hindsight, Reddy says that a better understanding of the market would have come in handy. “It would have actually helped us, rather than making an acquisition of that nature, overpaying, and then trying to make the best out of it. I think those assumptions and the learning before actually going about it are things that didn’t go very well,” he says.

Other cash-rich companies are also grappling with the consequences of shopping sprees. In the past seven years, Pune-based Bharat Forge made a bagful of acquisitions in Europe and the US to be closer to its customers and enhance service delivery. On 29 May, Bharat Forge said it was liquidating its loss-making plant and machinery in the US acquired from Federal Forge for US$9.1 million in 2005. After continued losses, the slowness of the revival at General Motors – a key Bharat Forge client – hit the company hard, according to Business Standard. Divesting the asset meant Bharat Forge would have no manufacturing unit in the US.

The company’s US acquisition was considered a good buy in 2005, but was a casualty of the global financial crisis.

Debts and patience

For many companies, outbound investments were either wayward or too expensive. “Some early outbound investments in mid-cap companies haven’t worked – their cash flows were not healthy and they lacked management bandwidth to turn it around,” says investment banker Rajeev Gupta, head of Arpwood Capital and the former managing director of Carlyle India.

The past few years saw Indian companies pile up huge debts to pick up assets globally. These deals have devastated buyers’ bottom lines, heightening investor caution. In early August, 6.6% was shaved off the market capitalization of the Indian telecom industry’s poster child, Bharti Airtel, after the company declared its results for the quarter ended 30 June. With a competitive domestic market, Bharti revealed that its African operations may not meet revenue and core earnings targets. Like most big acquisitions, the turnaround in Bharti Zain is taking time.

On 13 August, Indian wind turbine maker and supplier Suzlon Energy announced a net loss of US$154 million for the April-June quarter, compared with a profit of US$11 million in the corresponding quarter last year. A day later, the company’s scrip tumbled 3.95% despite its share value having already eroded 200% in the previous 12 months.

Suzlon, Asia’s third largest turbine player, had acquired Hamburg-based REpower Systems, a manufacturer of onshore and offshore wind turbines, over four years beginning 2007, piling up a debt of US$359 million. Struggling to pay off its debt, Suzlon is offloading its stake and divesting assets. In July, Suzlon founder chairman Tulsi Tanti said he was taking a 73% pay cut.

New directions

Despite a somewhat gloomy outlook, Gupta says companies are looking at overseas opportunities today because “investing in India is very painful and the outcomes are so uncertain”.

Indian investors still favour the US, UK and Asia as investment destinations (see Raffle prize, page 45). The diversified Sahara group is a case in point. It has been seeking a global footprint with interests as diverse as finance, housing and hotels.

Last year, Sahara, based in Lucknow in the northern state of Uttar Pradesh, gatecrashed into the global ring when it snapped up London’s Grosvenor House hotel from Royal Bank of Scotland for US$726 million. The property was valued at US$1.5 billion four years ago. Sahara agreed to buy a controlling stake in New York’s Plaza Hotel in July this year and is reported to be eyeing more Royal Bank of Scotland properties – a group of Marriot Hotels in London – for around US$1.18 billion.

The New York Times has reported that Sahara is also “said to be interested in other high-end hotel properties in New York, like the Four Seasons, the Mandarin Oriental and Waldorf-Astoria”.

Despite the popularity of the UK and US, Indian outbound investments over the past two years illustrate that many are willing to look beyond familiar territory for opportunities in European destinations such as Belarus, Bulgaria, Hungary, Poland, Russia and Slovenia, as well as in Australia, Canada, Latin America and Africa. Dealogic data show that in the past year, Australia led India outbound deals with US$2.08 billion followed by the US at US$1.74 billion and Europe at US$1.33 billion.

Europe has drawn Indian investments in a variety of industries.

While capital-intensive factories are being set up in central Europe, southern Europe has attracted auto component makers and auto design studios. Activity is also increasing in the chemicals and life sciences sector in Europe, while companies interested in renewable energy are tapping the UK’s solar power market.

India has lost some of its appetite for deals in Germany. “We are seeing Indian companies coming to Germany, setting up small outfits here to gain experience and then look for attractive targets,” says Klaus-Dieter Stephan, a partner and head of the India desk of Hengeler Mueller in Frankfurt. “Patience may be on the agenda more than quick large transactions.”

Stephan adds that with the comparatively strong state of the German economy, few assets are available at attractive prices.

In the Czech Republic, investments are being channelled into the steel industry and the manufacture of vehicles and ferries, says Radek Janecek, the managing partner at Squire Sanders’ Prague office. Investors also consider Slovakia’s market attractive for opportunities in car manufacturing, electrical and mechanical engineering, metallurgy and chemicals.

Ondrej Peterka, the managing partner at Peterka & Partners in Slovakia, says that Mahindra & Mahindra’s Reva Electric Car Company plans to invest €60 million (US$75 million) and create around 1,000 jobs to produce 30,000 cars a year in western Slovakia.

In Italy, M&A transactions have slowed but Indian companies are setting up subsidiaries for trading or research and development purposes and also branch offices, observes Arianna Carlotti, head of the India desk at Pirola Pennuto Zei & Associates in Rome. The firm has been engaged for disputes relating to “overdue payments, defective materials and the transfer of shares of Italian companies held by Indian shareholders,” she says.

For the past few years, African delegations have sought to generate interest among Indian companies in developing infrastructure, agricultural land and information technology in their nations. Africa consists of 54 countries with diverse mixes of political, cultural, religious and language factors, and different colonial backgrounds. The challenges investors face differ from country to country, but often the risks of investing in Africa are generalized, explains Robert Appelbaum, a senior partner and head of the South Asia group at Webber Wentzel in South Africa. “Every country is unique and should be approached as such, preferably using local knowledge and input,” he says.

Horses for courses

Speaking at the eighth India-Africa Project Partnership Summit in New Delhi in March this year, Anicet Parfait Mbay, minister of state for transport and civil aviation of the Central African Republic (CAR), said: “Being a landlocked country, CAR requires transportation which includes train, road and air networks. Raw material like ores and the mining industry cannot flourish if we do not have an efficient transport system to move these minerals out of mines and into factories.”

African nations presented business opportunities worth close to US$90 billion at the summit but investment by Indian companies in the past 12 months was only US$166 million.

“The challenge of structuring deals to comply with the black economic empowerment regulatory framework in South Africa is also one that is faced by potential investors from India,” says Appelbaum. “Unfortunately the concept has been seen by many Indian corporates as a major hindrance, and some have resorted to less than savoury practices to circumvent the requirements.”

John Ffooks, a senior partner at John W Ffooks in the CAR, says that being aware of the litigation consequences of resource nationalism among African states is important, and the international reach of anti-bribery and anti-fraud legislation brings additional risks.

Regulations may quickly become outdated too. Governments sometimes change regulations in response to public dissatisfaction with failures in current infrastructure – protests over energy cuts are one example – so when negotiating for future improvements to that infrastructure, performance guarantees are important.

“For French-speaking countries, most important is the membership, or otherwise, of a state in OHADA [Organisation pour l’Harmonisation en Afrique du Droit des Affaires],” says Ffooks. “OHADA enables legal recourse in commercial affairs over a wide range of potential business disputes, including arbitration as a means of dispute resolution.”

The challenge of financing

Every country has its own legal and regulatory challenges. In Europe, labour management and employment liabilities can be a challenge, making any kind of restructuring difficult. “Any proposed restructuring post-acquisition should be analysed threadbare before the acquisition,” says Mara at Osborne Clarke. “The acquiring management gives assurances as part of the deal that it will inject sufficient cash for the ailing company to be able to function post-acquisition. But funding can be an issue as there is a funding crunch in Europe and India, and the cost of finance in India is high.”

In addition, when Indian companies take loans from Indian banks to fund acquisition of assets across multiple jurisdictions, they give assurances to the lenders that they will pledge the target’s assets worldwide, including in the country where the target’s holding company is situated. If the holding company is in the UK, a problem may arise in France, which allows assets to be pledged only if a part of the loan is shown to come into a French company. If a loan goes to the UK, “assets in France cannot be pledged and the facility agreement with the bank lenders is breached,” explains Mara. “The options then are either for the borrower to pay off that part of the loan to the bank or for the bank to invoke a breach clause – both of which are messy.”

An investment in Italy requires careful due diligence on the target, focusing on the level of banking indebtedness, including the value of any derivatives transactions; litigation, tax liability and labour litigation, advises Carmelo Raimondo, the partner-in-charge of the India practice at Chiomenti Studio Legale in Milan. Additional issues include social security bilateral agreements, heavy taxation and labour costs. Investors may also have to contend with lengthy litigation in Italy.

All these challenges notwithstanding, lawyers say that Indian investments are much sought after. Says Ernst & Young’s Shah: “The capability of the Indians has been established. They are not going and buying for name’s sake but for business sense.”

[/ihc-hide-content]